Economic Empowerment - Part Three

Financial Literacy vs. Economic Empowerment (Part Three)

It's Not a Fair Fight!

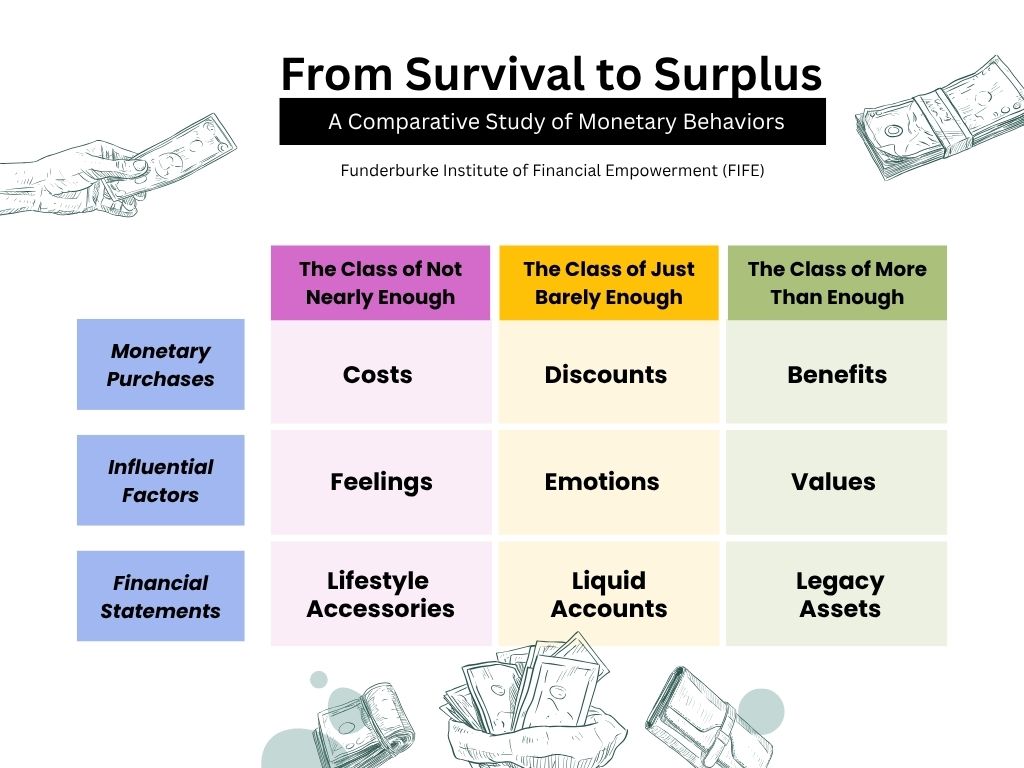

Costs. Discounts. Benefits. Feelings. Emotions. Values. Lifestyle Accessories. Liquid Accounts. Legacy Assets. When it comes to money, how you—or anyone else—use it speaks volumes about your financial mindset and class affiliation. In this third and final installment of the series, we’ll examine how social classes think, act, and behave economically in America and likely around the world. “Thinking” has everything to do with one’s thought process in dealing with money. “Acting” highlights how a person, couple, or family performs in handling financial matters, from calmness to anxiousness to ostentatiousness to unpretentiousness (and everything in between). “Behaving” underlies the ingrained habits, or default choices, that people make when allocating financial resources each month. One last point in this opening paragraph, and I’m paraphrasing a quote I heard one of my mentees share: Our financial frequently has everything to do with our economic frequency. And even if this is out of tune, we still march to the beat of its dictates anyway. I wrote about this phenomenon, and over 50 other social class comparisons, almost a decade ago in my book, Sociopsychonomics.

The Class of Not Nearly Enough

First up is the class of economic hardship, or those who’ve been dealt (often through no fault of their own) a bad financial hand in life. What’s so fascinating about working with groups on the fringes of society—which was my reality for nearly two decades—is that they tend to prioritize feelings over values, costs over benefits, lifestyles over legacies. It’s nearly impossible to break free from the shackles of economic bondage when instincts and impulses drive spending decisions. This is especially problematic when the pain and pressure of a brutal existence, coupled with inherited trauma, compels marginalized communities to live in, and only for, the present moment. Their response economically? Spend money, no matter the costs, on shoes, clothes, and other “outward” accessories to uplift their “inward” spirits. The problem? Debts accumulate on the liability side of the balance sheet, notably credit card charges and payday loan advances with every depreciating asset purchased. And so the vicious cycle of poverty continues, from one generation to the next.

The Class of Just Barely Enough

Property taxes have outpaced salary gains over the last several years. Grocery prices have continued to rise, even when supply has surpassed demand. Thanks to the law of diminishing returns, angst is in the air as blue-collar workers struggle to make ends meet—too few dollars to satisfy too many bills. They are stretched thin personally, professionally, and psychologically while trying to fund their middle-income lifestyle. Savings are being depleted. Job layoffs are starting to pile up. Doubts are drowning out the dreams of earning their fair share of the American pie. Fairness is not on the side of those who are caught in the crosshairs of having just barely enough. And their admirable work ethic, AWE for short, isn’t the leveraging tool that it once was in decades past. Employer-provided defined benefit plans (aka pensions) are all but gone; for the most part, they’ve been replaced by defined contribution plans (where the onus is now on employees to manage their own retirement accounts, in particular, risk-and-return tradeoffs in lieu of performance outcomes). Unlike the poor, there’s no social safety net for the middle class. Nope. But they do have a time sensitive, binary choice to make: get pushed down to the economic-hardship class, or move up to the appreciating-asset class. Tick tock.

The Class of More Than Enough

The good news is that the affluent class has added thousands of American households to this social strata of privilege over the last two decades. The bad news? Millions more are needed right now to close the wealth gaps in our country. Affluent-positioned Americans (APAs) place a premium on noteworthy benefits, value-driven principles, and legacy assets in accordance with their heritage script. Truth be told, this multilayered approach works for several reasons. First, they understand that the benefits received from a given product or service are worth the expense(s) made. Money is one thing, meaning is altogether different. Most APAs are purposeful in everything they do, including how they allocate financial resources; they don’t leave anything up for chance. Their world of investing is not confined just to certificate of deposits (CDs), stocks, bonds, mutual funds, and alternative investments. To them, getting a good deal isn’t about cost or a discount. It’s about their developmental advantages—what they gain, how they improve, where they excel, who they (or their children) become, and why they win. Time after time in their life and livelihood pursuits!

Second, values are the guiding principles that shape daily decisions, actions, and activities. Here’s the kicker: These tenets should be non-negotiable, regardless of one’s social class. If they aren’t, then they can’t be classified as values. Guiding principles serve many purposes, but chief among them is helping the wealthy avoid mission drift. As boundary markers and benchmark makers, values keep APAs in play when other social classes lose their way. Economic downtown? Stay the course. Political upheaval? Keep moving forward. Death in the family? Grieve as needed but stick to the written script. Third, legacy is arguably the most important component of the affluent-class playbook. Now, every individual or family leaves behind a legacy, but not every legacy is worth leaving behind. Sounds harsh, I know. But if an individual, couple, or family gets this wrong, benefits and values won’t matter. Why? Because there’s nothing to pass on to the next generation. No game plan. No goodwill. No great name. I pray that this three-part series has been a blessing to you. To our LFYO supporters and business partners, thank you for your generosity and hospitality in helping us equip and empower the least among us here in Central Ohio.

Exciting News!

Coming Next Week!

Stay tuned for our upcoming 2026 Fundraising Luncheon announcement, where we will unveil this year’s keynote speaker and host location.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us for our annual fundraiser! We’re passionate about equipping the next generation with the tools they need to go from just 'knowing' about money to truly mastering their economic future.

Related Articles

Economic Empowerment - Part Two

Financial Literacy vs. Economic Empowerment (Part Two)

It's Not a Fair Fight!

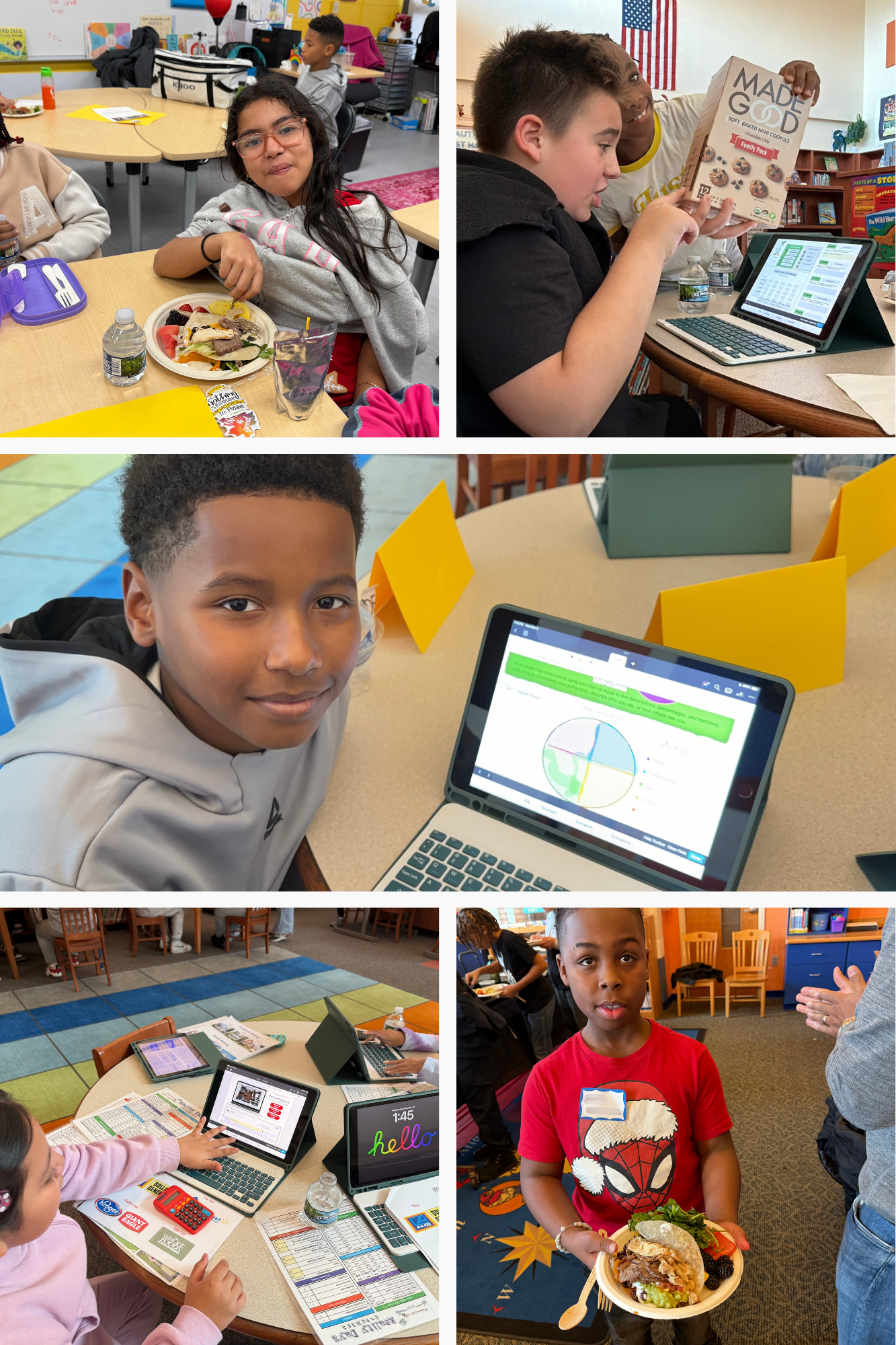

Start the course in childhood, continue the journey throughout adulthood. Developing financial life skills within the framework of wealth-building initiatives—investing in stocks, bonds, mutual funds, and other compounding-growth options—are critical to helping at-risk youth connect the academic and opportunistic dots. Yes, these concepts are foreign to most fifth-grade students (regardless of their family’s economic situation). But an introduction to personal finance should come sooner rather than later for children from under-resourced households. They’re quite familiar with the typical, outdated motivational track: Go to school. Secure a job. Earn an income. With some minor revising and major revealing, vulnerable students should have access to this updated, twenty-first century educational template: gain a foundational understanding of wealth-building principles in elementary school; identify talents, gifts, and abilities in middle school that align with a child’s mission-driven fit; and create a pathway for high schoolers to become philanthropic contributors as change-agent specialists within their respective communities. When high-need students experience the miscues of financial mismanagement and the virtues of wealth accumulation firsthand in game-based settings, they’re generally more aware and excited about their future prospects and place in this world.

Not Nearly Enough vs. Just Barely Enough vs. More Than Enough

One of the biggest mistakes middle-class facilitators in the financial literacy field or educational arena make when working with low-income households is this: They often place limits on how far up the economic ladder the less fortunate (as well as members of their own social class clique) can climb. Surface-level mantras, even innocent ones, do more harm than good. “Get a safe and secure job.” “Stick to a realistic budget.” “Be careful investing; it’s not that much different than gambling.” You get the picture. Safe and secure jobs don’t exist anymore in our modern, AI- and algorithm-driven world. Workforce cracks, aka seismic shifts in the (un)employment landscape, are just around the corner. Budgeting is so passé, so why not highlight cash flow management instead? The former is suffocating, while the latter is liberating. Yes, semantics matter a great deal when financial freedom is on the line. True enough, speculative investing is akin to gambling. However, calculated risk taking—when guided by and guarded with due diligence—is not. As any value investor knows who typically pays more attention to balance sheets than income statements (when evaluating prospective companies), extensive research is the key to finding good stocks selling at a steep discount to their intrinsic value or fundamental worth.

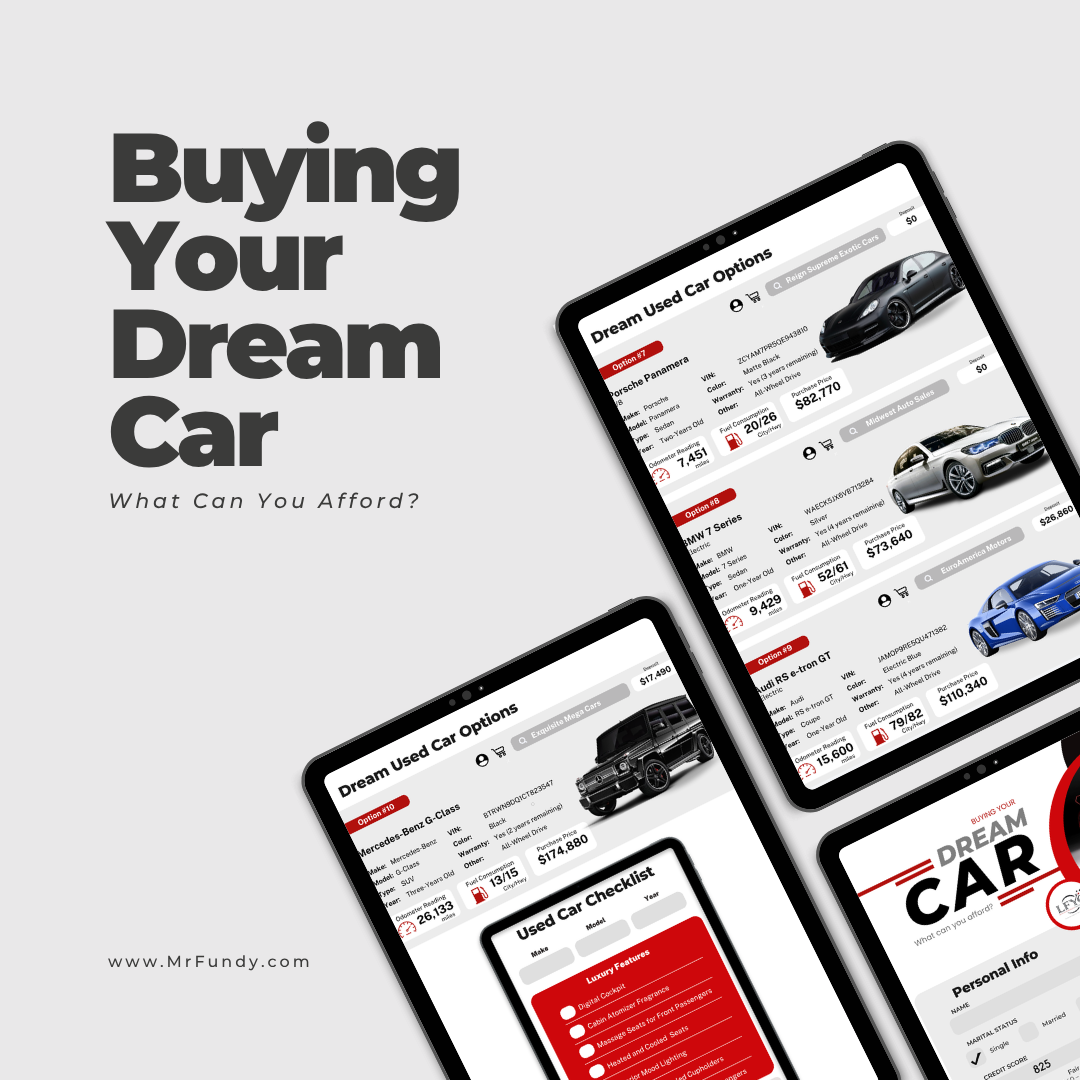

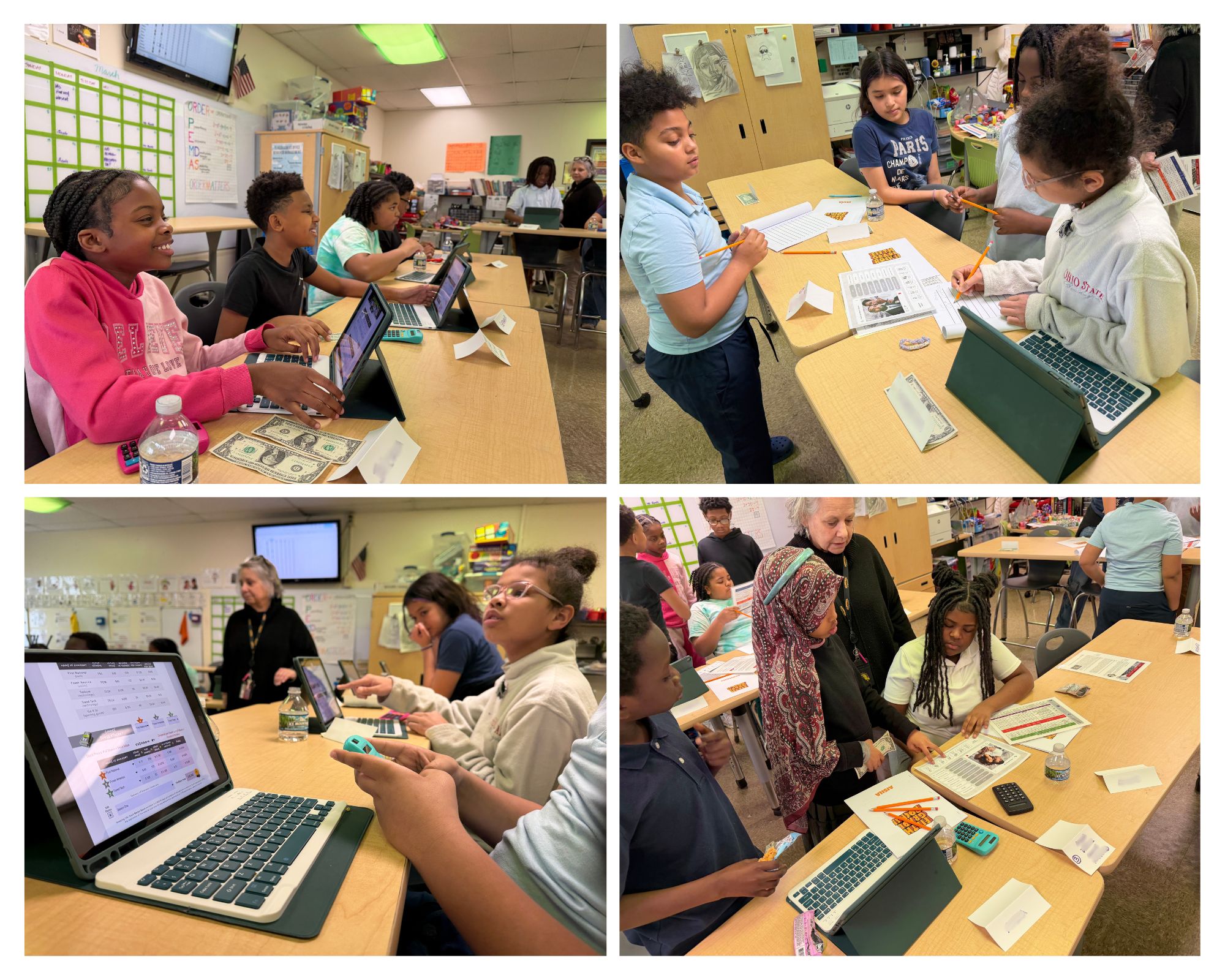

In settings using make-believe money, vulnerable students should dream big. In our Buying Your Dream Car activity, we allow underserved youth to reach for the stars. In this interactive exercise using an iPad, students are assigned a hypothetical occupation, monthly salary, marital status, credit score, and balance sheet to purchase their dream car. The experience even includes step-by-step instructions on financing considerations, notably making a down payment or placing a deposit, buying an extended warranty, and selecting the number of monthly payments until the bank loan is repaid. Luxury vehicle selections are as follows: Range Rover Sport, Mercedes-Benz Maybach, Bentley Flying Spur, Ferrari Spider, Lamborghini Urus, Tesla X, Porsche Panamera, BMW 7 Series, Audi RS e-tron GT, and a Mercedes-Benz G Wagon. While scrolling through the list of dream cars, the collective oohs and aahs of students is music to our ears. The acoustics and optics in the classroom are why we, Monya and I, do what we do as economic empowerment crusaders. Create an enriching environment—through gamification activities—that places each student in the driver’s seat of holistic success. As tour-guide representatives, it’s incumbent upon us (like teachers, principals, and administrators) to provide inner-city youth with the navigational aptitude needed to achieve a prosperous life with legacy benefits.

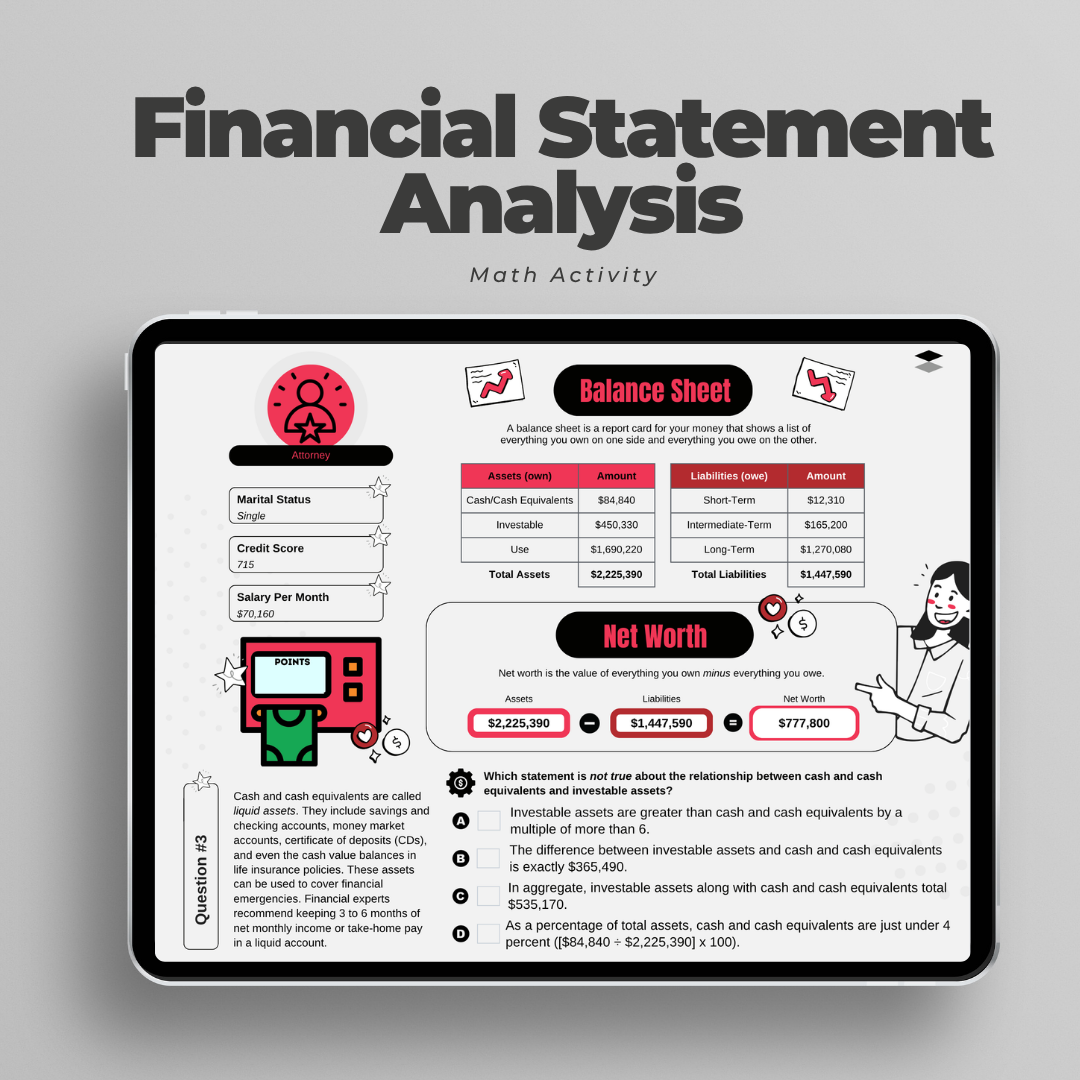

In closing, choice architecture (along with consequence assessment) is the name of the life improvement game for at-risk communities, who often choose the path of least resistance when they can’t opt out of higher-level thinking while evaluating mentally challenging strategies. Here’s what I’ve learned as a non-traditional educator and certified financial planner over the last 15 years: Data processing can quickly turn into information overload for vulnerable students who are short on academic conditioning. And when fatigue sets in, disinterest levels ramp up. The remedy? Provide a constant supply of stimulating flashpoints that connect inner-city students’ present reality (personal boredom) with their future possibility (financial freedom). A well-timed break to serve healthy snacks helps too! You see, the dream car they desire to purchase down the road comes with a hefty price tag. Whether it’s a car, house, or stock investment, everything has a cost. Pay now, play later. Play now, pay later. That choice, even by default, is theirs to make—whether they realize it or not. And reminding LFYO participants what could be and how they can achieve it is rooted in biochemical tuning. “Pay-careful-attention” comments boost norepinephrine or concentration levels. “Imagine-what-life-will-be-like-when-you’re-net-worth-is-off-the-charts” reflections increase serotonin or feel-good levels. “Stay-with-it” promptings amplify their endorphin or resiliency levels. Without question, neurotransmitter development is the most important factor in helping inner-city students step outside their math sweet spot and into their computational growth zone through personal finance concepts. And friction is required for this to occur! We have included a page from one of our financial math worksheets below for your review. Keep an eye out for part three in this economic empowerment series, which I’ll release next week. Until then, stay blessed.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us for our annual fundraiser! We’re passionate about equipping the next generation with the tools they need to go from just 'knowing' about money to truly mastering their economic future.

Related Articles

Economic Empowerment - Part One

Financial Literacy vs. Economic Empowerment (Part One)

It's Not a Fair Fight!

Financial literacy is incriminating, highlighting where people fall short in the area of basic, money management habits. But economic empowerment is liberating, showcasing who they can become as wealth-building accumulators and legacy-minded progenitors.

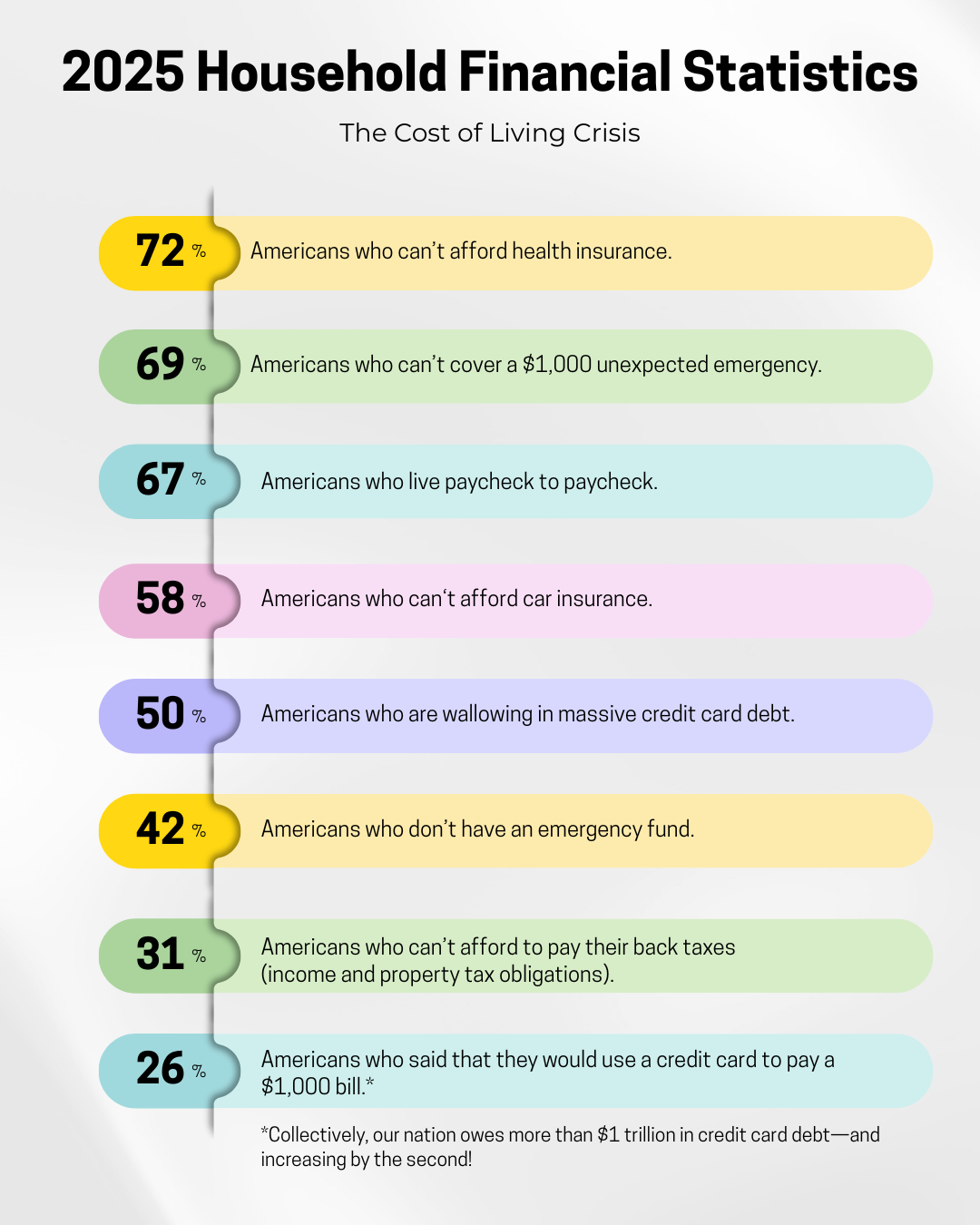

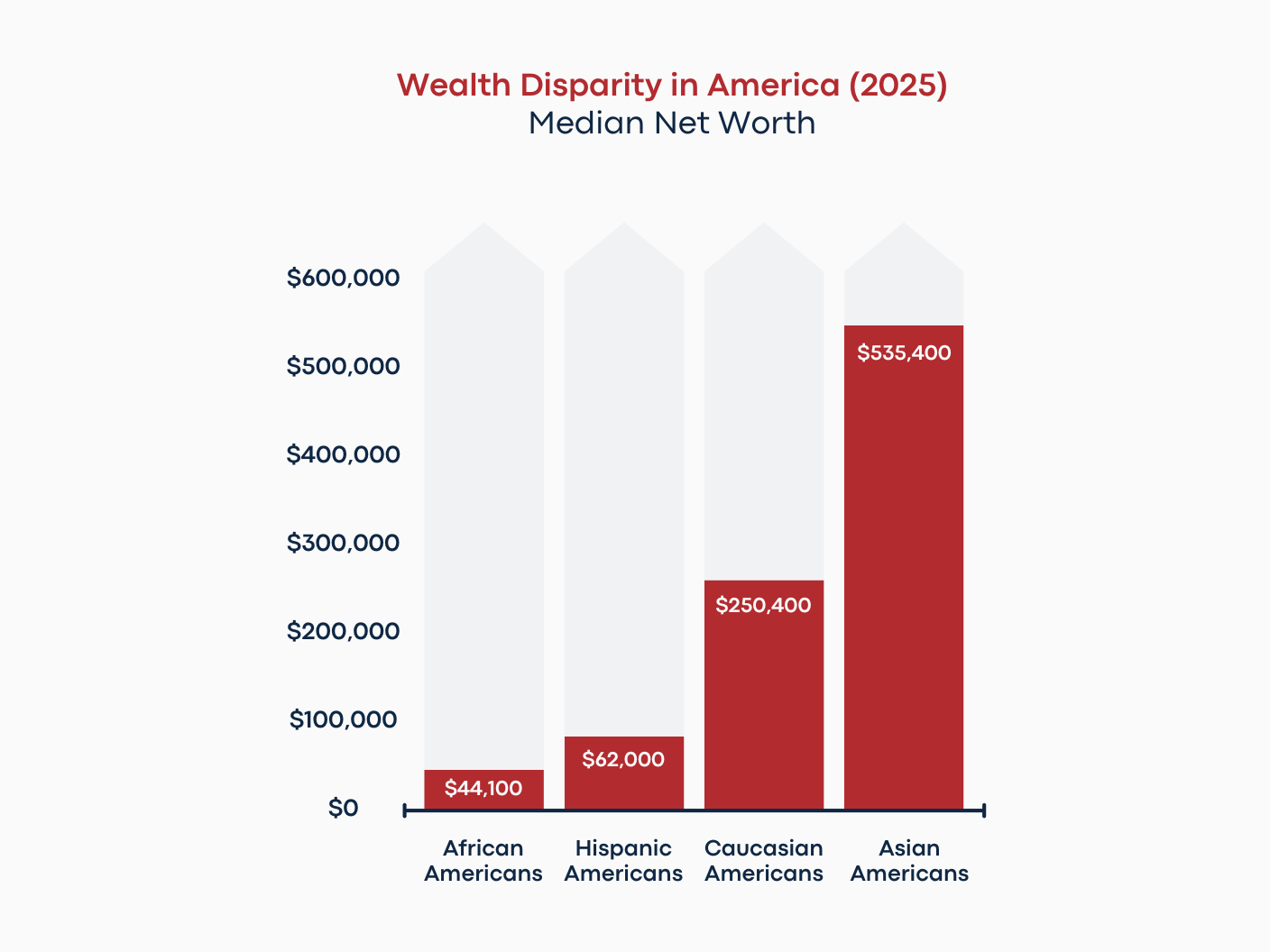

April is National Financial Literacy Month. Great optics, lackluster semantics. Translation: Placing a monthlong spotlight on helping Americans develop better financial habits is definitely needed. However, equipping them with the mindset and skillset to build wealth is absolutely necessary. Here’s why. The state of wealth among racial groups, which the Covid pandemic exacerbated, should be our collective wake-up call. Black and brown communities are way behind financially. According to the Pew Research Center, the median net worth of African Americans in 2025 was $44,100. For Hispanics, their balance sheet was slightly stronger at $62,000. The net worth of white households was around $250,400, almost six times higher than their African-American counterparts. In comparison to Asian Americans, the wealth picture is even bleaker for black and brown families. Asian Americans have a median net worth of $535,400, 12 times greater than African Americans and roughly nine times more than Hispanic Americans.

This disparity in wealth is quite troubling on several fronts. First, children from asset-deprived households often see their economic world from a glass half-empty perspective. Second, this life outlook can, and usually does, lead to self-defeating attitudes and self-sabotaging behaviors that result in self-fulfilling prophecies guided by this pessimistic belief system: “Fate is not on our side; we can never bend the odds of financial success in our favor!” Third, fatalism inevitably pulls high-need communities toward gambling traps and lottery pitfalls—or other get-rich quick, desperation schemes—to cover the shortfall. These speculative outlets, which are often fueled by superstitious hunches and “lucky break” mantras, end up causing more financial pain than they alleviate. That’s why LFYO offers a downstream playbook to deal with this upstream problem across the age spectrum.

In our Investing 101 app-based game, we teach fifth-grade students who attend inner-city schools the basics of asset allocation, stock market investing in particular. (Asset allocation is the process of spreading investment funds among various risk-and-reward options, such as savings and checking accounts, certificate of deposits, stocks, bonds, mutual funds, and nontraditional offerings.) After a brief discussion on the risk-and-return profile of several mainstream investment categories, students test their skills as newbie investors. We keep things simple in this introductory game; only five options are available. One bank stock. One utility stock. Two technology stocks. One sporting goods stock. Participants select three out of the five for their $15,000 portfolio, or $5,000 for each selection. I ask the class, “Are you ready to make some real money with your knowledge?” I then follow up with, “Can you name a publicly traded bank or financial institution?” Hands immediately shoot up in the air, and each correct answer is rewarded with a dollar. “Huntington Bank.” “Chase Bank.” “Bank of America.” “Fifth Third Bank.” “Key Bank.” The same question is asked about utility, technology, and sporting goods stocks. I close out the investing session with this statement, “You can make money in an up, down, or sideways stock market.” Lesson learned by the fifth graders; the down payment to get them fired up about their financial future has been made. Here’s a fact that is rarely considered by residents in low-income communities: They walk inside or drive past the brands of publicly traded companies everyday without even realizing it—shopping malls, grocery stores, and gas stations, to name just a few. Thus, wealth-building opportunities are hidden in plain sight from them. As U.S. congresswoman Joyce Beatty pointed out to me over a decade ago, “Black and brown Americans can’t just be on the customer side of the cash-register equation. They also need to be on the owner and investor side, too!” Great advice.

Recently, we facilitated a classroom simulation with fifth graders, where each team served as financial planners by committee for five hypothetical clients, three couples and two individuals. Students provided their investment recommendations (in the form of asset allocation strategies) for clients based on risk tolerance (conservative, moderate, or aggressive), time horizon (or when a client plans on withdrawing income from the portfolio), and estimated annual return on investment (ROI) projections. From low- to high-risk selections, investment options were as follows: savings and checking accounts, money market accounts, certificate of deposits (CDs), government and corporate bonds, mutual funds, value and growth stocks, real estate properties, hedge funds, private equities, precious metals, and crypto currencies. In terms of suitability, investment options were aligned with each client’s risk tolerance ahead of time, but the fifth graders did have the liberty to allocate the $1,000,000 as they chose. Their math challenge? Make sure the numbers, fractions, and percentages correctly added up when presenting their recommendations in front of the class. Sounds like a lesson too big for eleven-year olds from disadvantaged backgrounds to handle. Nothing could be further from the truth. In fact, they even exceeded our loftiest expectations during their presentations, which is why members on the winning team each won $20. Stay tuned for Part II in this economic empowerment series.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us at our annual fundraiser as we equip the next generation with the tools to transition from financial literacy to true economic power.