Financial Literacy vs. Economic Empowerment (Part One)

It's Not a Fair Fight!

Financial literacy is incriminating, highlighting where people fall short in the area of basic, money management habits. But economic empowerment is liberating, showcasing who they can become as wealth-building accumulators and legacy-minded progenitors.

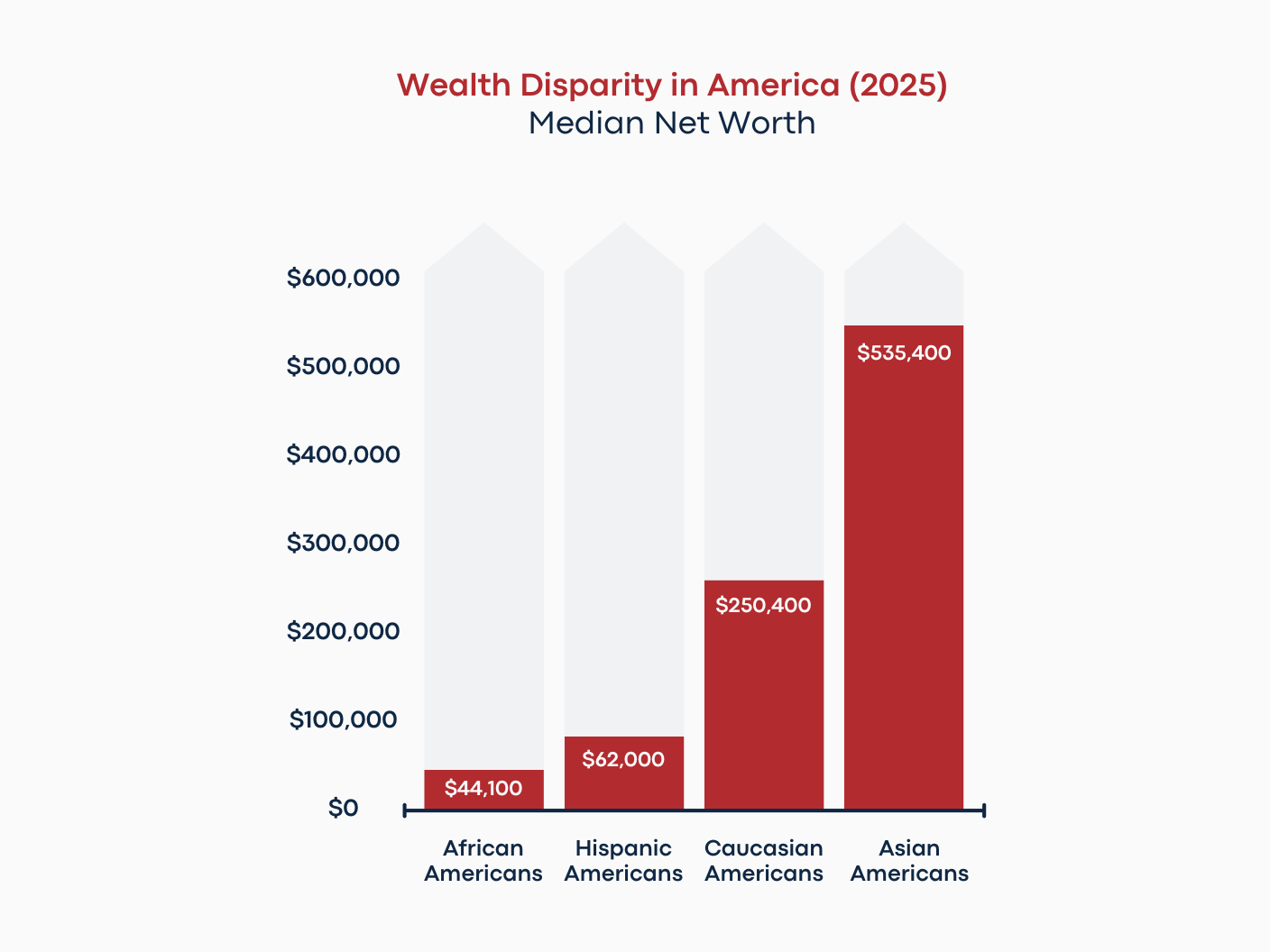

April is National Financial Literacy Month. Great optics, lackluster semantics. Translation: Placing a monthlong spotlight on helping Americans develop better financial habits is definitely needed. However, equipping them with the mindset and skillset to build wealth is absolutely necessary. Here’s why. The state of wealth among racial groups, which the Covid pandemic exacerbated, should be our collective wake-up call. Black and brown communities are way behind financially. According to the Pew Research Center, the median net worth of African Americans in 2025 was $44,100. For Hispanics, their balance sheet was slightly stronger at $62,000. The net worth of white households was around $250,400, almost six times higher than their African-American counterparts. In comparison to Asian Americans, the wealth picture is even bleaker for black and brown families. Asian Americans have a median net worth of $535,400, 12 times greater than African Americans and roughly nine times more than Hispanic Americans.

This disparity in wealth is quite troubling on several fronts. First, children from asset-deprived households often see their economic world from a glass half-empty perspective. Second, this life outlook can, and usually does, lead to self-defeating attitudes and self-sabotaging behaviors that result in self-fulfilling prophecies guided by this pessimistic belief system: “Fate is not on our side; we can never bend the odds of financial success in our favor!” Third, fatalism inevitably pulls high-need communities toward gambling traps and lottery pitfalls—or other get-rich quick, desperation schemes—to cover the shortfall. These speculative outlets, which are often fueled by superstitious hunches and “lucky break” mantras, end up causing more financial pain than they alleviate. That’s why LFYO offers a downstream playbook to deal with this upstream problem across the age spectrum.

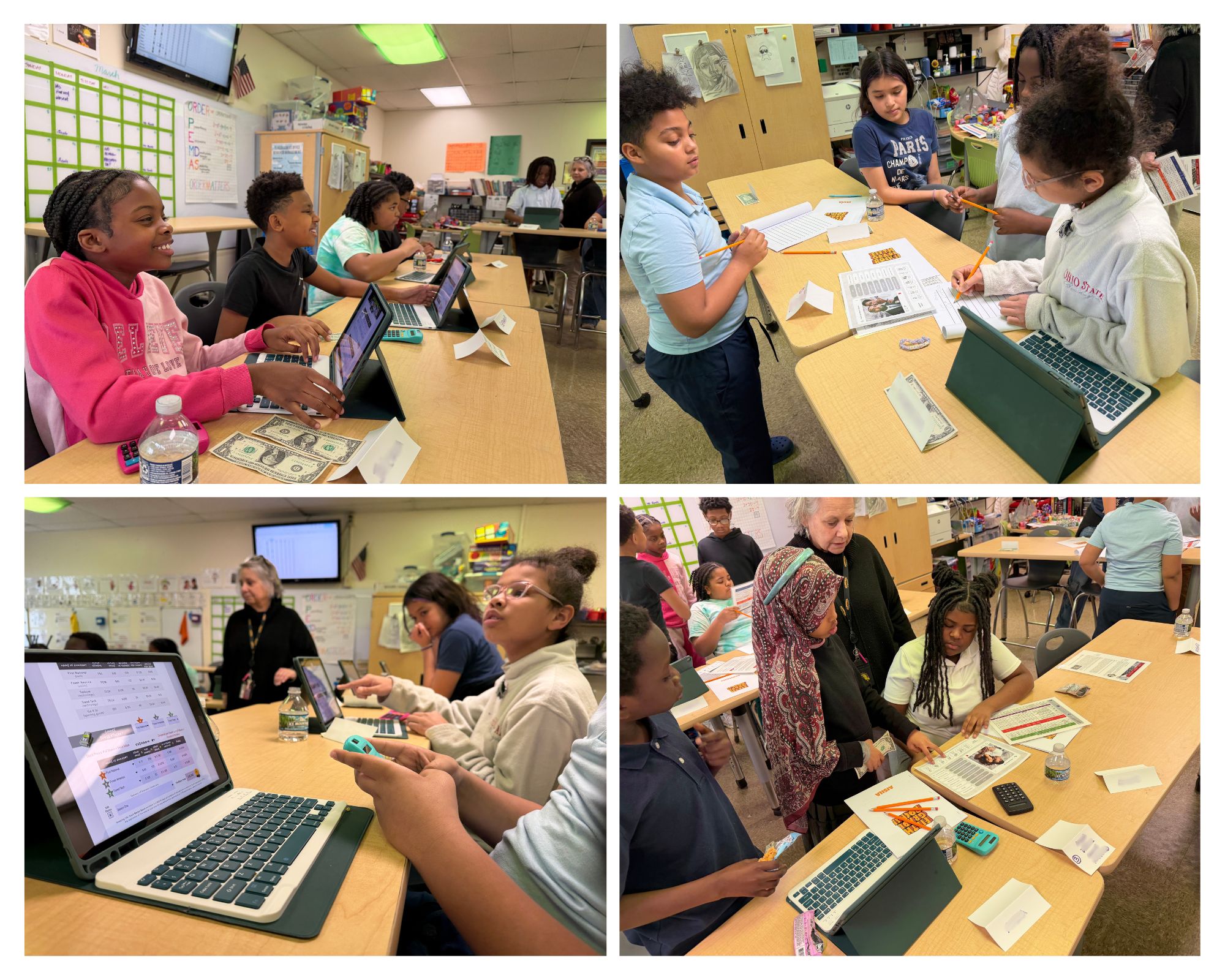

In our Investing 101 app-based game, we teach fifth-grade students who attend inner-city schools the basics of asset allocation, stock market investing in particular. (Asset allocation is the process of spreading investment funds among various risk-and-reward options, such as savings and checking accounts, certificate of deposits, stocks, bonds, mutual funds, and nontraditional offerings.) After a brief discussion on the risk-and-return profile of several mainstream investment categories, students test their skills as newbie investors. We keep things simple in this introductory game; only five options are available. One bank stock. One utility stock. Two technology stocks. One sporting goods stock. Participants select three out of the five for their $15,000 portfolio, or $5,000 for each selection. I ask the class, “Are you ready to make some real money with your knowledge?” I then follow up with, “Can you name a publicly traded bank or financial institution?” Hands immediately shoot up in the air, and each correct answer is rewarded with a dollar. “Huntington Bank.” “Chase Bank.” “Bank of America.” “Fifth Third Bank.” “Key Bank.” The same question is asked about utility, technology, and sporting goods stocks. I close out the investing session with this statement, “You can make money in an up, down, or sideways stock market.” Lesson learned by the fifth graders; the down payment to get them fired up about their financial future has been made. Here’s a fact that is rarely considered by residents in low-income communities: They walk inside or drive past the brands of publicly traded companies everyday without even realizing it—shopping malls, grocery stores, and gas stations, to name just a few. Thus, wealth-building opportunities are hidden in plain sight from them. As U.S. congresswoman Joyce Beatty pointed out to me over a decade ago, “Black and brown Americans can’t just be on the customer side of the cash-register equation. They also need to be on the owner and investor side, too!” Great advice.

Recently, we facilitated a classroom simulation with fifth graders, where each team served as financial planners by committee for five hypothetical clients, three couples and two individuals. Students provided their investment recommendations (in the form of asset allocation strategies) for clients based on risk tolerance (conservative, moderate, or aggressive), time horizon (or when a client plans on withdrawing income from the portfolio), and estimated annual return on investment (ROI) projections. From low- to high-risk selections, investment options were as follows: savings and checking accounts, money market accounts, certificate of deposits (CDs), government and corporate bonds, mutual funds, value and growth stocks, real estate properties, hedge funds, private equities, precious metals, and crypto currencies. In terms of suitability, investment options were aligned with each client’s risk tolerance ahead of time, but the fifth graders did have the liberty to allocate the $1,000,000 as they chose. Their math challenge? Make sure the numbers, fractions, and percentages correctly added up when presenting their recommendations in front of the class. Sounds like a lesson too big for eleven-year olds from disadvantaged backgrounds to handle. Nothing could be further from the truth. In fact, they even exceeded our loftiest expectations during their presentations, which is why members on the winning team each won $20. Stay tuned for Part II in this economic empowerment series.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us at our annual fundraiser as we equip the next generation with the tools to transition from financial literacy to true economic power.