Financial Literacy vs. Economic Empowerment (Part Three)

It's Not a Fair Fight!

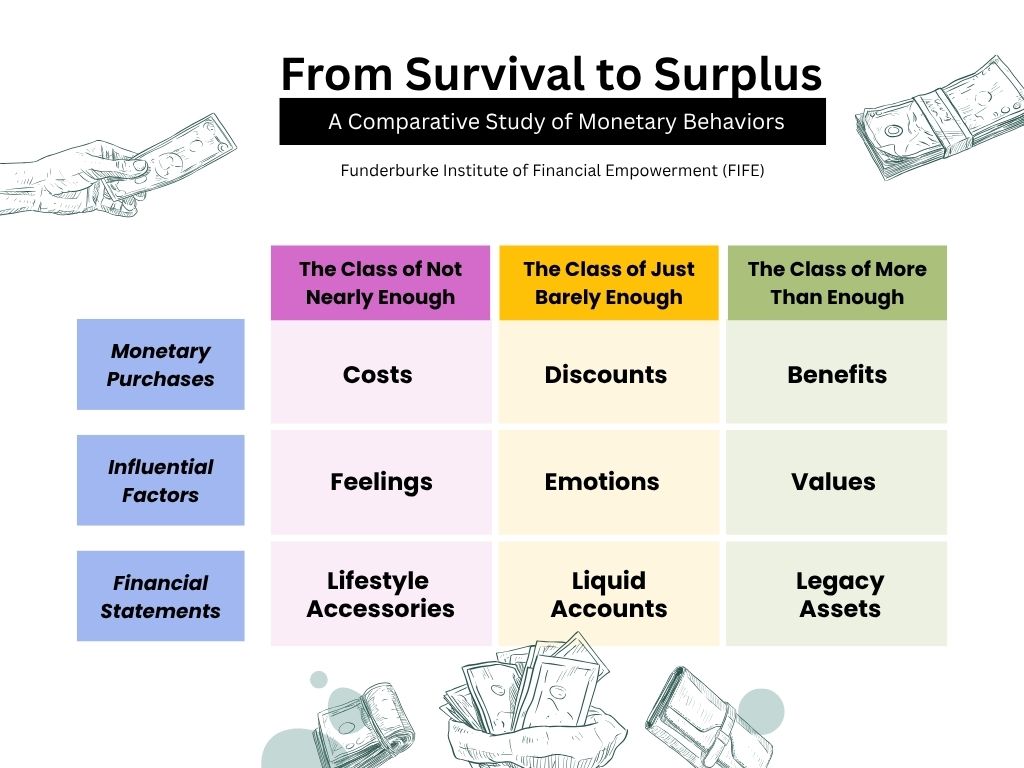

Costs. Discounts. Benefits. Feelings. Emotions. Values. Lifestyle Accessories. Liquid Accounts. Legacy Assets. When it comes to money, how you—or anyone else—use it speaks volumes about your financial mindset and class affiliation. In this third and final installment of the series, we’ll examine how social classes think, act, and behave economically in America and likely around the world. “Thinking” has everything to do with one’s thought process in dealing with money. “Acting” highlights how a person, couple, or family performs in handling financial matters, from calmness to anxiousness to ostentatiousness to unpretentiousness (and everything in between). “Behaving” underlies the ingrained habits, or default choices, that people make when allocating financial resources each month. One last point in this opening paragraph, and I’m paraphrasing a quote I heard one of my mentees share: Our financial frequently has everything to do with our economic frequency. And even if this is out of tune, we still march to the beat of its dictates anyway. I wrote about this phenomenon, and over 50 other social class comparisons, almost a decade ago in my book, Sociopsychonomics.

The Class of Not Nearly Enough

First up is the class of economic hardship, or those who’ve been dealt (often through no fault of their own) a bad financial hand in life. What’s so fascinating about working with groups on the fringes of society—which was my reality for nearly two decades—is that they tend to prioritize feelings over values, costs over benefits, lifestyles over legacies. It’s nearly impossible to break free from the shackles of economic bondage when instincts and impulses drive spending decisions. This is especially problematic when the pain and pressure of a brutal existence, coupled with inherited trauma, compels marginalized communities to live in, and only for, the present moment. Their response economically? Spend money, no matter the costs, on shoes, clothes, and other “outward” accessories to uplift their “inward” spirits. The problem? Debts accumulate on the liability side of the balance sheet, notably credit card charges and payday loan advances with every depreciating asset purchased. And so the vicious cycle of poverty continues, from one generation to the next.

The Class of Just Barely Enough

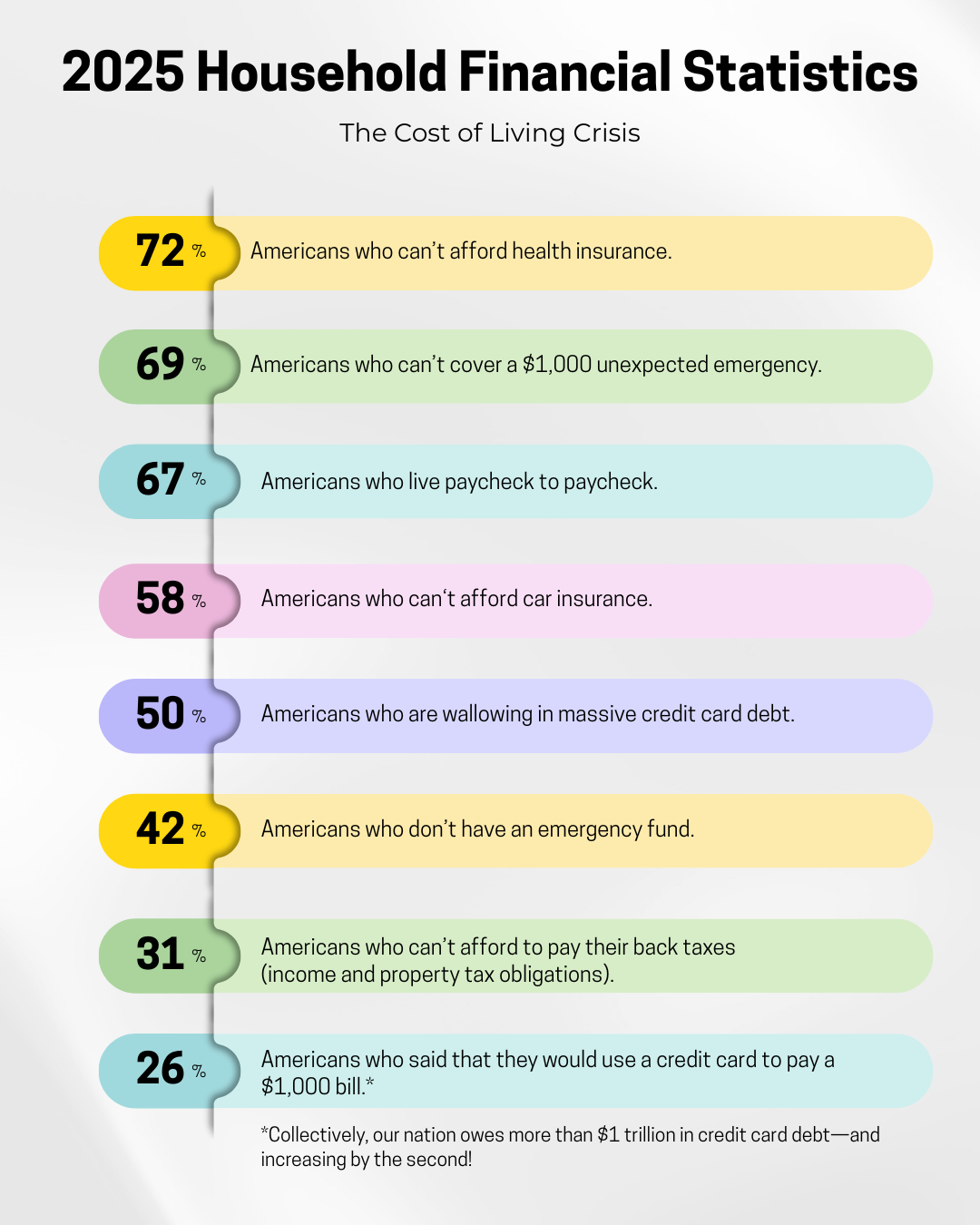

Property taxes have outpaced salary gains over the last several years. Grocery prices have continued to rise, even when supply has surpassed demand. Thanks to the law of diminishing returns, angst is in the air as blue-collar workers struggle to make ends meet—too few dollars to satisfy too many bills. They are stretched thin personally, professionally, and psychologically while trying to fund their middle-income lifestyle. Savings are being depleted. Job layoffs are starting to pile up. Doubts are drowning out the dreams of earning their fair share of the American pie. Fairness is not on the side of those who are caught in the crosshairs of having just barely enough. And their admirable work ethic, AWE for short, isn’t the leveraging tool that it once was in decades past. Employer-provided defined benefit plans (aka pensions) are all but gone; for the most part, they’ve been replaced by defined contribution plans (where the onus is now on employees to manage their own retirement accounts, in particular, risk-and-return tradeoffs in lieu of performance outcomes). Unlike the poor, there’s no social safety net for the middle class. Nope. But they do have a time sensitive, binary choice to make: get pushed down to the economic-hardship class, or move up to the appreciating-asset class. Tick tock.

The Class of More Than Enough

The good news is that the affluent class has added thousands of American households to this social strata of privilege over the last two decades. The bad news? Millions more are needed right now to close the wealth gaps in our country. Affluent-positioned Americans (APAs) place a premium on noteworthy benefits, value-driven principles, and legacy assets in accordance with their heritage script. Truth be told, this multilayered approach works for several reasons. First, they understand that the benefits received from a given product or service are worth the expense(s) made. Money is one thing, meaning is altogether different. Most APAs are purposeful in everything they do, including how they allocate financial resources; they don’t leave anything up for chance. Their world of investing is not confined just to certificate of deposits (CDs), stocks, bonds, mutual funds, and alternative investments. To them, getting a good deal isn’t about cost or a discount. It’s about their developmental advantages—what they gain, how they improve, where they excel, who they (or their children) become, and why they win. Time after time in their life and livelihood pursuits!

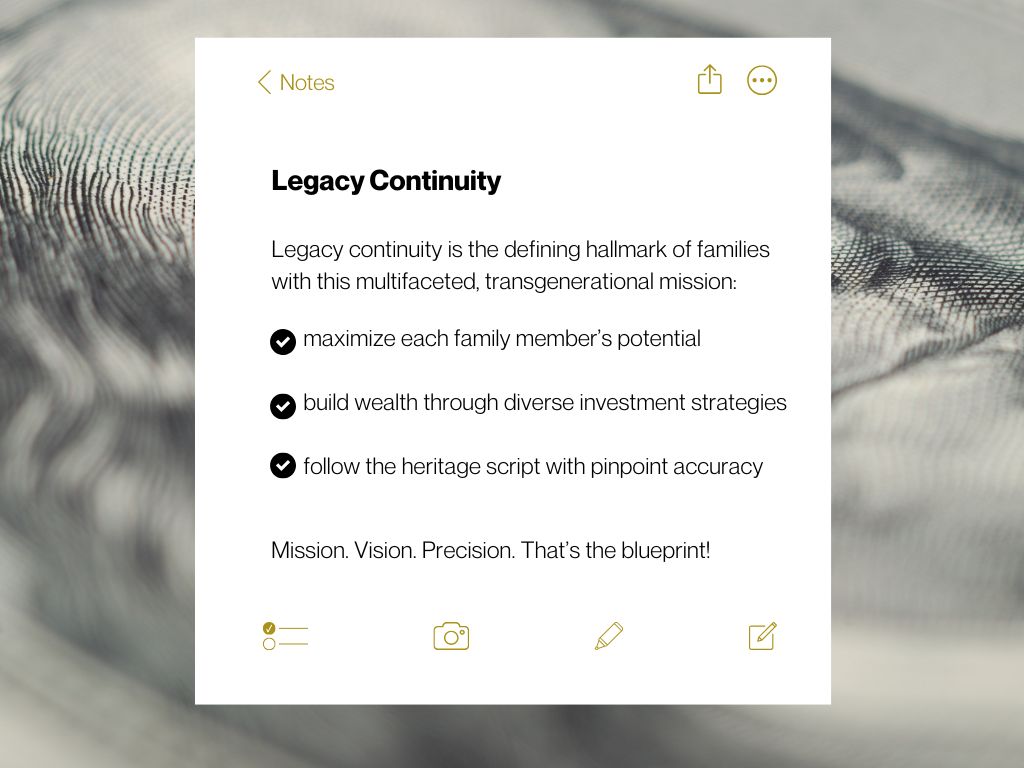

Second, values are the guiding principles that shape daily decisions, actions, and activities. Here’s the kicker: These tenets should be non-negotiable, regardless of one’s social class. If they aren’t, then they can’t be classified as values. Guiding principles serve many purposes, but chief among them is helping the wealthy avoid mission drift. As boundary markers and benchmark makers, values keep APAs in play when other social classes lose their way. Economic downtown? Stay the course. Political upheaval? Keep moving forward. Death in the family? Grieve as needed but stick to the written script. Third, legacy is arguably the most important component of the affluent-class playbook. Now, every individual or family leaves behind a legacy, but not every legacy is worth leaving behind. Sounds harsh, I know. But if an individual, couple, or family gets this wrong, benefits and values won’t matter. Why? Because there’s nothing to pass on to the next generation. No game plan. No goodwill. No great name. I pray that this three-part series has been a blessing to you. To our LFYO supporters and business partners, thank you for your generosity and hospitality in helping us equip and empower the least among us here in Central Ohio.

Exciting News!

Coming Next Week!

Stay tuned for our upcoming 2026 Fundraising Luncheon announcement, where we will unveil this year’s keynote speaker and host location.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us for our annual fundraiser! We’re passionate about equipping the next generation with the tools they need to go from just 'knowing' about money to truly mastering their economic future.