Gambling Addiction (Part III)

Wasted Lives, Wrecked Legacies

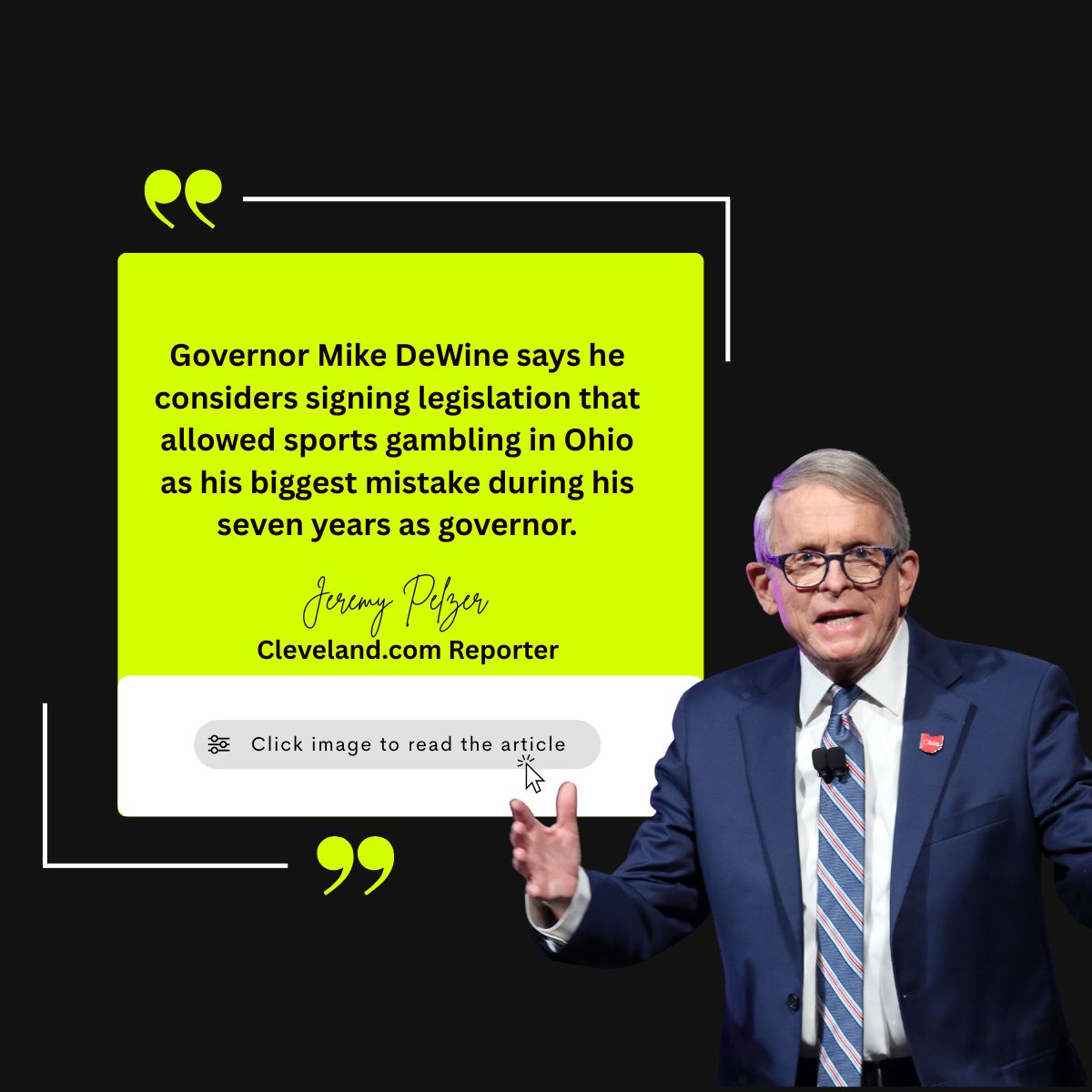

The fate of most problem gamblers who aren’t able to break free from their sports-betting addiction is some combination of a shortchanged life and a short-circuited legacy. Living is what they lose (in addition to a lot of money), and heritage is who suffers close to them (as a result of compulsive gamblers’ forfeited meaning or purposeless existence). Money lost, meaning less. And Ohio Governor Mike DeWine is intimately familiar with the personal brokenness journey behind the legislation he signed into law in 2021 but didn’t take effect until 2023. His jaw-dropping admission is one of the most shocking mea culpas I’ve ever heard a politician share in a public or private forum. I do applaud Governor DeWine for admitting his mistake, especially when so many gambling addicts have squandered their savings or home equity lines of credit, sabotaged their once-thriving marriages, and some have even taken their own lives. It’s so sad. On the sports side, Northeast Ohio native, Terry Rozier, tops the list. This former star basketball player at Shaker Heights High School and current NBA player (on suspended leave) has been implicated in a federal gambling probe. Two Cleveland Guardian pitchers, Emmanuel Chase and Luis Ortiz, were caught rigging pitch counts. Several University of Dayton basketball players faced threats from disgruntled sports gamblers. Brendan Sorsby, the star quarterback at Cincinnati over the past two seasons, admitted to placing thousands of sports bets while in college. (Sorsby has since transferred to Texas Tech; he did check himself into a residential treatment facility to address his gambling addiction.) Now think about how bad the side effects of sports gambling are for Ohio’s general population! Let’s discuss a few of them.

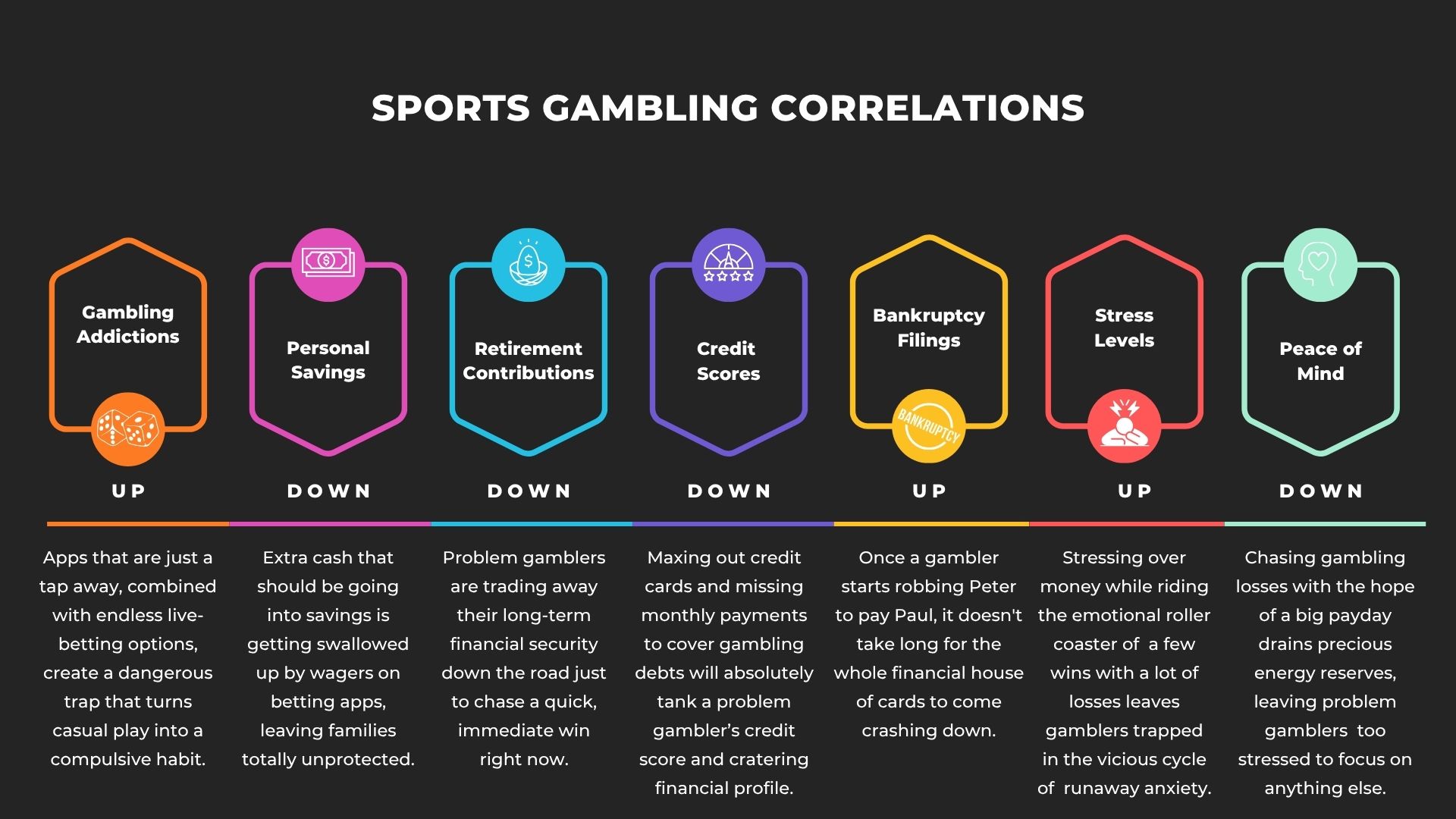

Side Effect #1: Financial Distress

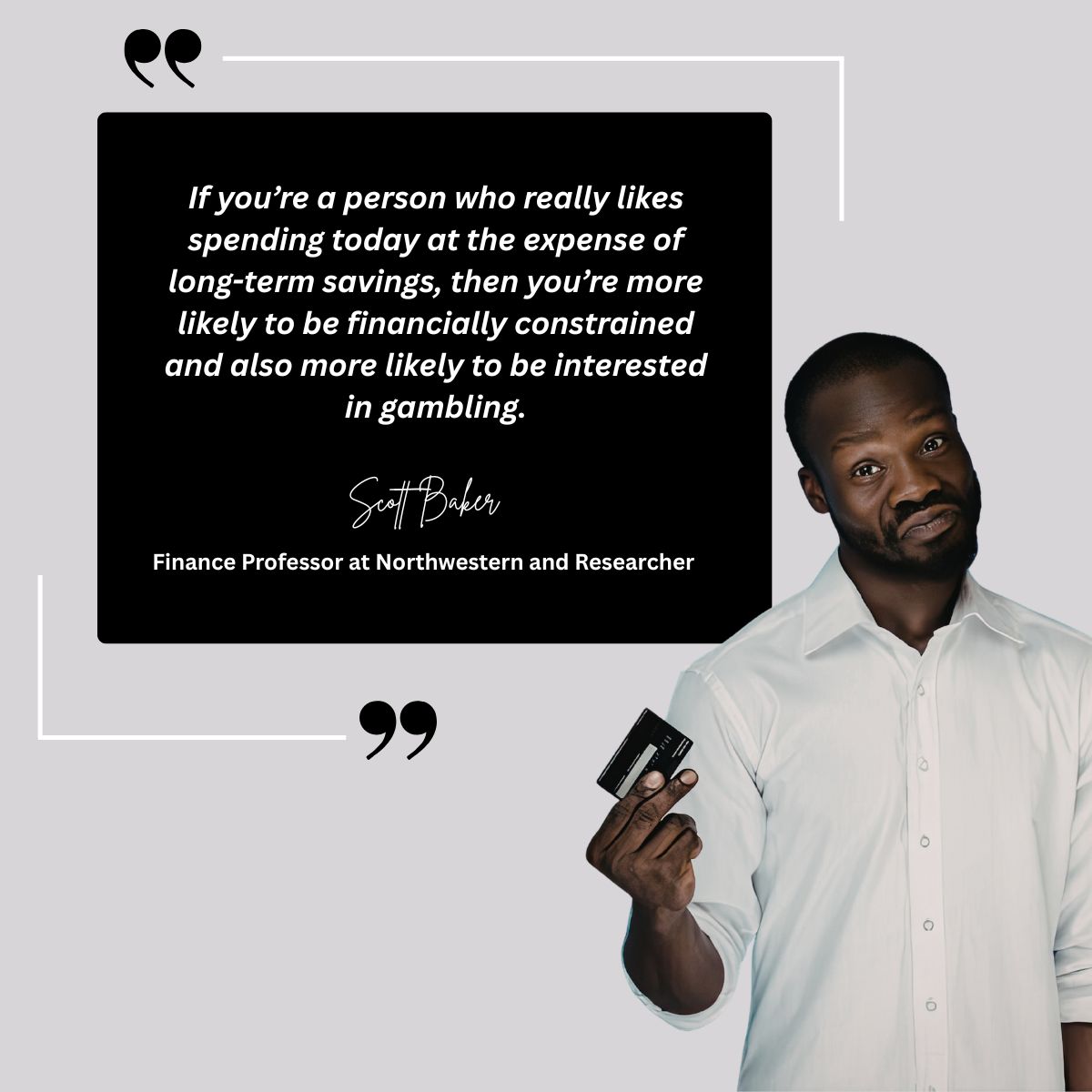

Throwing good money at incredibly bad odds is a painful lesson in futility. For most sports gamblers, chasing that next high will typically result in suffering through a new low. That new low—and the desperate measures that follow—has a ripple effect on personal or family finances for months (or even years) to come. “It’s a huge problem among young males up to 45,” Governor DeWine says. “And many of them are addicted, many of them spending money that they do not have.” Check this out. A groundbreaking study tracked the damage sports gambling has had in America over a five-year period from 2018 to 2023. Scott Baker, a finance professor at Northwestern University’s Kellogg School of Management and lead researcher, shared the following five conclusions, among others:

-

Researchers saw that nearly 8 percent of households were involved in some form of gambling.

-

While the amount of money people put into legal sports gambling rose, their net investments fell by nearly 14 percent.

-

For every $1 a household spent on betting, it put $2 fewer into investment accounts.

-

Evidence suggests greater access to sports gambling increased general participation in lottery games, particularly among households that frequently overdraw their bank accounts.

-

Beyond this, sports gambling also led to increased spending on cable TV, restaurants, and other forms of entertainment—possibly, the researchers speculate, driven by a greater engagement with live sporting events.

https://insight.kellogg.northwestern.edu/article/online-sports-betting-is-draining-household-savings

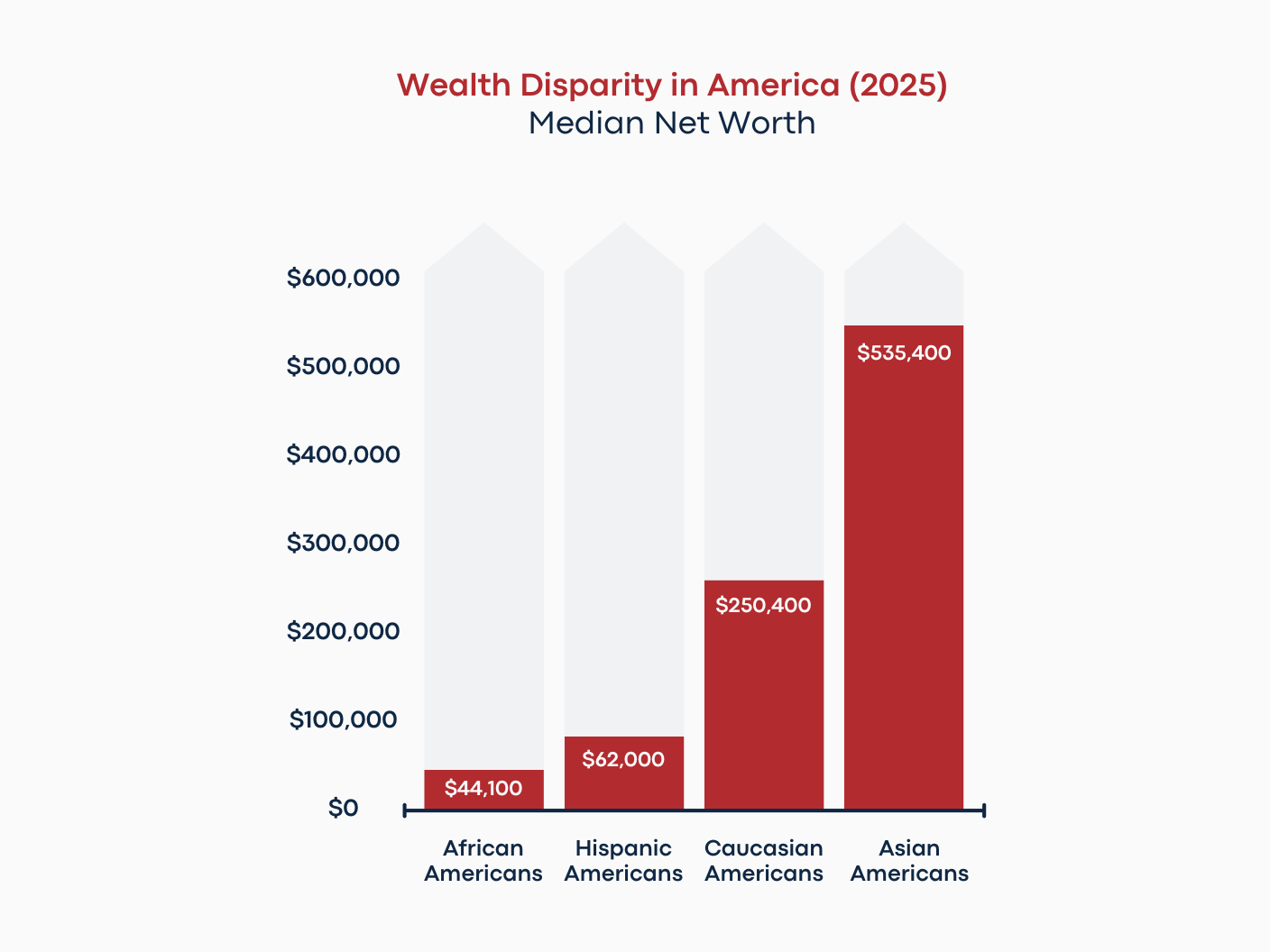

We, as a collective group, don’t have any money to waste. African Americans are at the bottom of the economic rung, with gambling debts and lottery losses adding to our shared misery. For every Oprah and Jay Z, we have Pookie and Ray Ray, Shamika and Sha Nay Nay. (By the way, my oldest niece is named Shamika.) As a community, we’re way behind financially when viewed from the prism of median net worth: $44,100 (African Americans), $62,000 (Hispanic Americans), $250,400 (Caucasian Americans), $535,400 (Asian Americans). We spend more on food, clothing, and entertainment than any other ethnic group. We contribute the least to our 401k retirement accounts than any other ethnic group. We are more prone to get-rich-quick schemes that promise huge payouts on small wagers than any other ethnic group. The 2022 census shared a shocking finding. Almost a quarter of black households had a negative to zero net worth compared to whites at 8.6 percent. So many ex-pro athletes and mega-paid celebrities claim to be pro black, but their endorsement deals with gambling companies contradict what they actually promote. Many of them were on the front lines of the Black Lives Matter Movement, but shouldn’t Black Legacies Matter More from an economic empowerment perspective? We’re quick to protest an unjust capitalistic system (and rightly so at times), but why are we setting up our own people for failure who gamble away money they can least afford to misspend? For African Americans, affinity bets using the advice of famous people who look, sound, and act like us do more harm than good. Sports gambling wagers should instead be redirected to fund 529 college savings accounts, increase contributions to retirement plans, start new businesses, make homeownership down payments, and more importantly, empower inner-city black youth through holistic initiatives.

Side Effect #2: Relational Distrust

Addiction found, trust lost. Troublesome measures are pursued by gambling addicts to cover their tracks in a relationship. As betting losses pile up, they must lie, hide, and/or steal to cover up the facade. Lying, hiding, and stealing are default responses that wounded players often display in the hurting games. Lie about the problem. Hide from personal responsibility. Steal from his, really their, financial future. To settle the score from the lost-bet scars—in their mind—all that’s needed is a big payout from the next wager. Unfortunately, problem gamblers end up digging an even deeper hole for themselves as well as the innocent bystanders around them. They not only lose more money; even worse, they mismanage relational capital with loved ones who feel betrayed. For many unsuspecting thrill-seekers who gamble, they are unaware of this roller-coaster outcome: The highs of relational deposits in the distant past are superseded by the lows of relational distrust in the present moment. Can the relationship recover? I guess it depends on two key factors, the gambling addict’s willingness to change and whether a loved one whose been deeply hurt has the heart to forgive. Both are required to build meaningful trust again, and they must occur simultaneously.

Jordan Acer (pronounced “Aker”), a certified financial planner and co-owner of Concordia Wealth Planning, has worked with hundreds of clients over his 10-year career. In a phone interview, he shared insights on several clients who’ve dealt with gambling struggles under his financial guidance. Acer points out, “When clients are withdrawing more than the plan is allowing, we, as planners, can highlight this in a loving way. But it’s their money, not ours.” He adds, “What ends up happening for some clients is that they’ll set up two separate financial planning accounts. Of course, this allows the husband to hide the gambling addiction from his wife.” He continues, “She knows when her husband is at the casino or a sports bar betting on games. His whereabouts are pinged by the location finder on her phone.” Trust is lost as the problem gambler burns through life savings, home equity lines, and retirement accounts to place ongoing bets. Wives or significant others don’t want to compete against an all-consuming gambling addiction; they want to be wholeheartedly pursued. Acer mentioned a close friend and problem gambler who stopped returning his calls, went through a difficult divorce, and moved out of state away from his kids. He notes, “And this phenomenon of relational distance has accelerated since sports gambling became legal in Ohio.” Unless something drastically changes on the legislative front, this will get far worse for those inside and outside the Buckeye state who are impacted by the side effects of gambling addictions.

Side Effect #3: Biochemical Disturbance

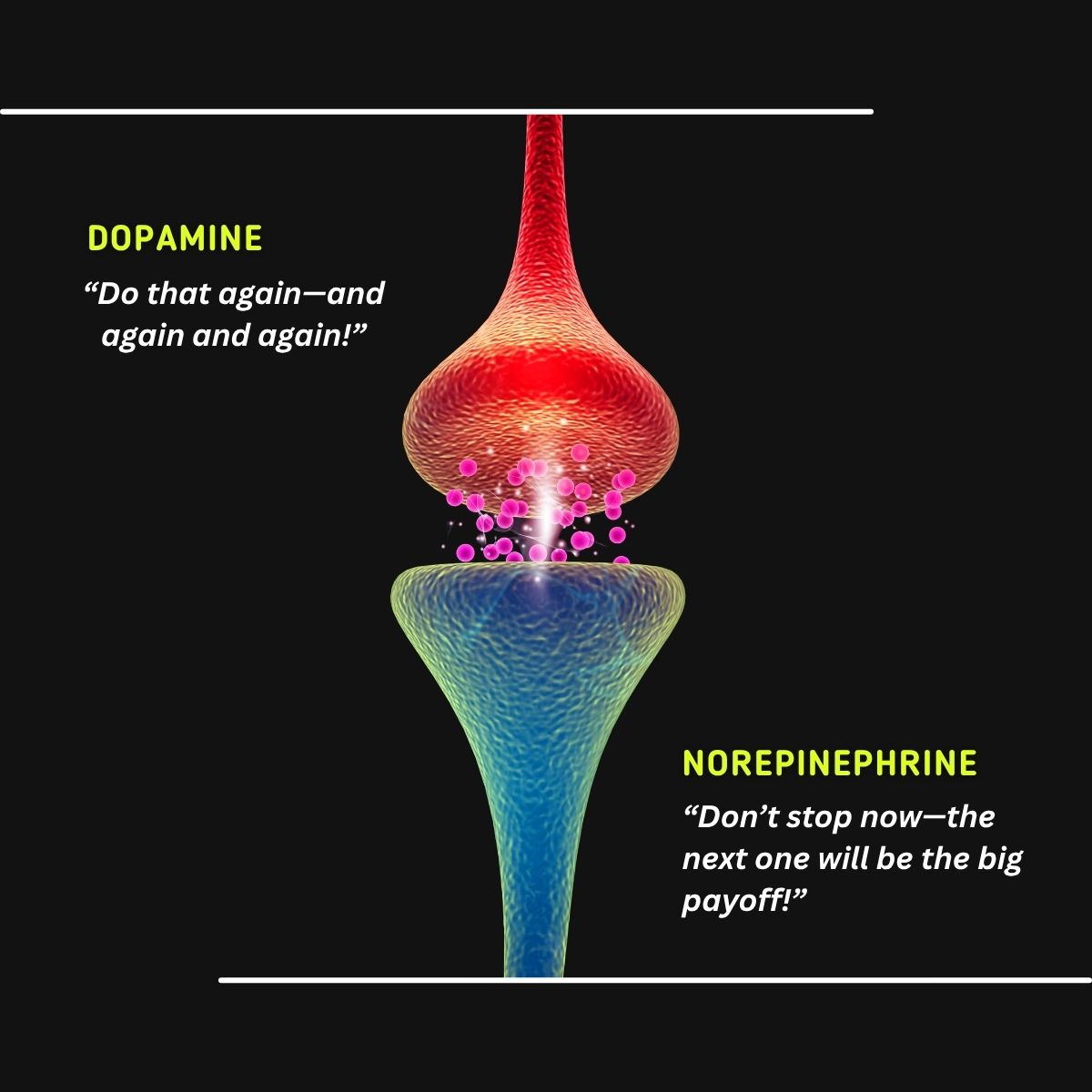

I know this to be true about addiction: the body doesn’t differentiate; it only responds. Doesn’t matter the addiction, the body is conditioned (through the reward pathway system) to replicate that initial high or low when the dopamine alert bells scream, “Do that again—and again and again!” And dopamine isn’t the only biochemical expression at play. A worn-out body needs a constant jolt of hyper-vigilance to keep a sports gambling addict locked in to the next wager. Norepinephrine, also known as noradrenaline, shows up and shows out with a vengeance. This excitatory neurotransmitter keeps the gas pedal on full throttle for problem gamblers who need every ounce of concentration from one bet to the next. It won’t let them miss out on a betting opportunity from sun up to sundown, whether it’s a west coast a west coast NBA playoff game or a table tennis tournament on the other side of the globe. There’s no rest for weary sports gamblers operating on fumes. They can’t deviate off course; norepinephrine, and it’s sidekick glutamate, won’t let them.

We can’t apply a bandaid to a gambling addict who is hemorrhaging from a wounded past. No, we must first offer a bandwidth solution, hopefully through the guidance of a qualified addiction counselor. Let me explain. Bandwidth is about tuning in to that gambling addict’s frequency meter or station of pain, say 106.5, where he plays or places 106 bets in 5 minutes by running from that permanent hurt to find his temporary relief. What permanent hurt? Being abandoned by his biological parents as a kid and shuffling between one foster care home to the next. Getting bullied on social media back in high school. Falling short as a misguided son, indecisive husband, or nonexistent father. The incessant betting is the remedy for his background noise or station of pain. (This also applies to females with gambling problems.) You see, most of us, if we’re honest, have background noise in our lives. We worry. We criticize. We doubt. The likely cause? Insecure attachments that still haunt us to this day, those maternal and/or paternal relationship deficits in childhood that follow us to adulthood. Experiences that aren’t even remembered before the age of six can negatively affect us decades later (Reference #1). Remember “Ryan” in the second article of this series? Well, he was born by Cesarean section; he also wasn’t breastfed as a baby. He admits, “I’ve always struggled with attachment issues as a teenager and young adult” (Reference #2). I’d venture to say that in the majority of cases, the roots of parental harm cause or greatly contribute to the offshoots of biochemical damage that lead to obsessive thoughts, compulsive tendencies, and addictive behaviors in children as they age.

Reference #1

Santiago Delboy. How Childhood Trauma Becomes Part of Who We Are as Adults. The origins of people pleasing, self doubt, shame, disassociation, and more. Psychology Today. March 31, 2025.

Reference #2

Marie-Andree Grisbrook and colleagues. The Association between Cesarean Section Delivery and Child Behavior: Is It Mediated by Maternal Post-Traumatic Stress Disorder and Maternal Postpartum Depression? January 17, 2024. NIH. National Library of Medicine.

Chasing Money, Losing Meaning

Regardless of the addiction, a life assignment has to be part of the remedy for those caught in the grips of one. And people who are guided by purpose don’t gamble with their money when meaning is on the line. Think about that for a moment. I define purpose as the assignment you were placed on this earth to accomplish for the benefit and betterment of others. With any life assignment, you’re going to have pop quizzes and open-book tests for growth-oriented purposes. And when chasing a lot of money, it’s easy to lose out on meaning. How so? Well, the allure of capitalizing on an improbable chance leads to getting caught up in a never-ending choice. What really happens is that problem gamblers lose the power of choice. You can only opt in to the next wager, not out of it. For gambling addicts, the choice is never binary (0 for not betting and 1 for the next bet). Because when choice is driven entirely by chance, which is the case with a gambling addiction, your life is operating in reverse order. This obviously will have a negative impact on a problem gambler’s circadian rhythm (how your body’s frequency or tuning system operates over a 24-hour period) and circaseptanrhythm (how in tune your life operates over an extended period of time, say 5 to 7 days). These two systems must be operating at peak efficiency for an individual to have a legitimate chance at fulfilling a purpose-centered, life assignment. And one of the telltale signs of a gambling addiction is a disrupted and dysregulated circadian rhythm. That’s when other vices show up—drinking, drugging, and drifting—to make up for the biochemical shortfall. This can lead to deep depression and suicidal ideation as losses mount. (The suicide continuum consists of fantasizing planning, vacillating, attempting, and completing self-inflicted death.)

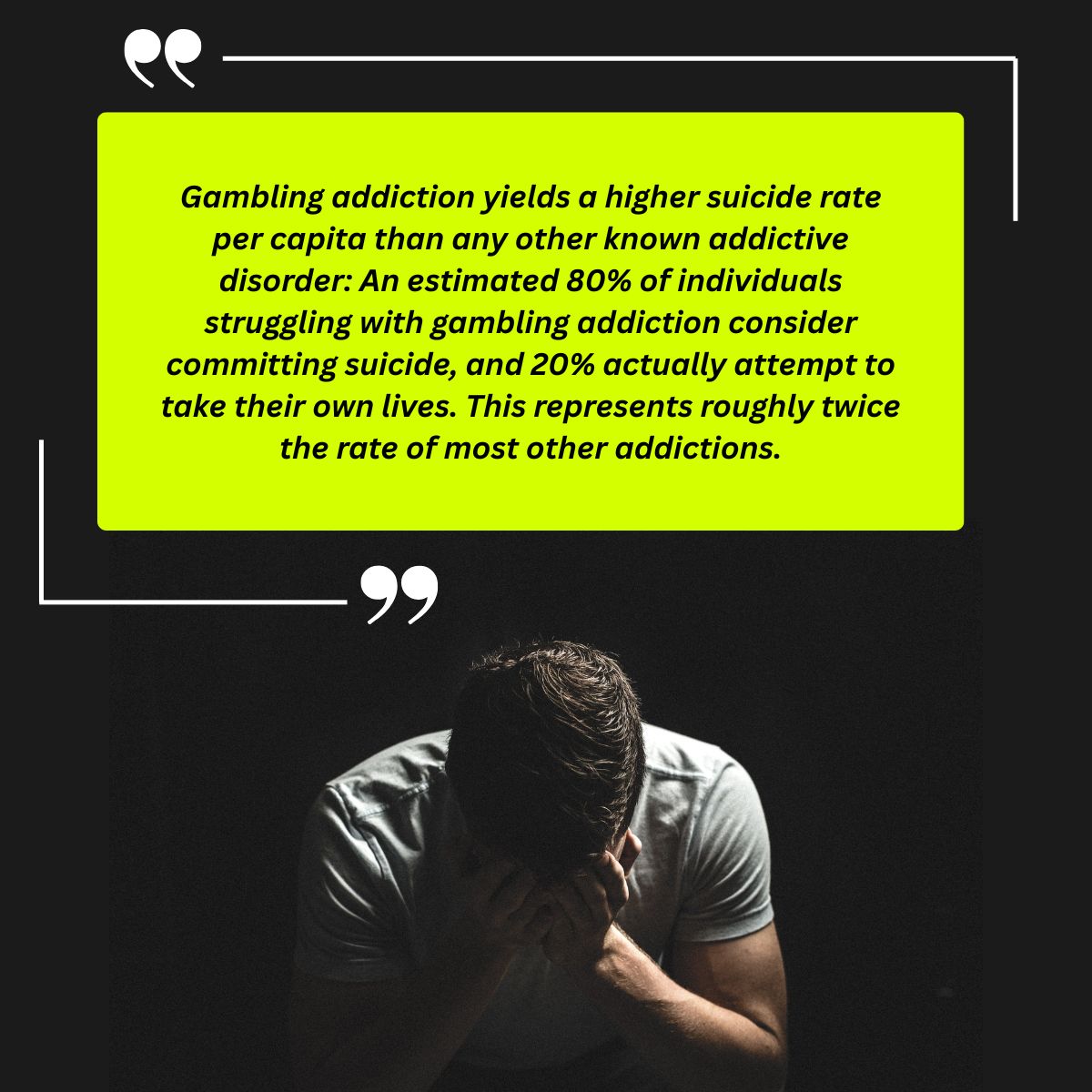

Let me close out the series with this heartbreaking stat from Ohio’s Casino Control Commission website:

Recent Articles

Gambling Addiction (Part II)

Cracking the Gambling Addiction Code

An algorithmic node—that’s what a problem gambler is—in the addiction network. Online sports gambling is a significant part of the prediction economy, a system in which future (or even split-second live) bets can result in lucrative payoffs for an infinitesimally small number of winners. The problem is not with the anticipated gain; it’s the assumption that somehow a loss will be altogether avoided, or worse, not considered at all. Here’s what I mean. In order for the sports gambling system to capture pools of willing players, significant amounts of data have to be collected on “monetized targets,” notably where they live, play, and work; who they follow in the sports world; why they enjoy live betting more than static gambling; when they’re likely to place small, medium, or large bets; how frequently they wager over a given time period; and which mix of parlays or prop bets are most appealing to them, among many other considerations. What gambling addicts don’t realize is this: the very same information they voluntarily share in responding to an affinity-based questionnaire or on a rapport-building phone call will, at some point, be used for their own demise. I call this the entrapment of systemic risk. Stay with me now. In effect, every sports gambler’s individual risk (and affinity, VIP profile) is added to the group’s mutual risks. The problem? Betters rarely share in collective gains but do quite often participate in cumulative losses through the law of large numbers. And when gamblers try to walk away from impulsive betting, frequency capital will be used to reel them back in. Managing moods is the biochemical manipulation key bookmakers deploy to unlock, really extract, more and more money from out-of-tune gamblers.

Sports bets are often made on the basis of superstitious beliefs, lucky hunches, past performances, forecasted trends, and of course, expert opinions (thanks, in large part, to celebrity endorsements from retired pro athletes and comedy icons). You see, the currency of assurance is the insurance of conviction. And this is precisely why gambling companies pay influential voices—who often leverage their larger than life colorful personalities or comedic routines in scripted, attention-grabbing advertisements—a boatload of money. The outlay is certainly worth the investment from a return-on-capital perspective. It’s a brilliant marketing tactic using an incredibly deceptive entrapment practice. This practice, among others, is what keeps gambling addicts locked into a game with bad outcomes. Pay up. Play on. Pray for. That next winning bet! By the way, humor influences human emotion and distorts logical thinking, serving as an embellishment hook to draw people in rather than to push them away. Don’t ask questions, just laugh at the joke, flow with the skit, embrace the punchline, and forget your problems. But there’s nothing funny about losing a job, spouse, or worse, a loved one through suicide due to a runaway gambling addiction.

“He’s Feeling It!”

I’m a big fan of Carmelo (Mr. Cool) Anthony. I followed him at Syracuse, where he lead the Orangemen to a 2003 National Championship as a freshman. The Hall of Fame legend and three-time Olympic gold medalist had an illustrious NBA career. He scored 28,289 points in 19 NBA seasons. As the ultimate “Shot Hunter” and “Bucket Maker,” his confidence in scoring timely baskets was second to none. In our modern era, MJ was certainly next level, Kobe was a close second, and Kevin Durant right behind him. But Anthony could give all three of these all-world scorers a run for their money as the crème de la crème in making sure that spherical ball went through that orange hoop. With pinpoint accuracy! What I especially admired about Anthony was his ability to score—at will—on all four Olympic teams. Different makeup, same outcome. No matter who was on the floor with him, he knew how, where, and when to get his points. That’s why his insights carry a lot of weight as an NBC-Peacock basketball analyst for NBA games. During halftime of the fourth NBA playoff game between the Detroit Pistons and Cleveland Cavaliers, Anthony’s commentary on live player props for DraftKings caught my attention. Regarding Caris LeVert, a reserve player for the Pistons who scored 17 points in the first half, Anthony emphatically stated that LeVert would easily score more than the prop betting line, 23+. “All, that’s easy; he will get that in the third quarter!” LeVert had 22 points by the end of the third quarter, and finished with 24 for the game. Here’s the question to ask: How many viewers were persuaded by Anthony’s insights to bet on LeVert scoring more than 23 points before the start of the second half? Probably a lot.

The lure of predictive betting is very tempting to pass up. As noted in Part I of this series, I’m not a gambler. However, I do make predictive forecasts all the time as a former NBA player while watching college or pro basketball games. Because I am keenly familiar with the psychology and physiology of the sport, I do have “inside information” at my disposal. Through a production (more than a prediction) lens, I observe players’ and coaches’ body of work in previous games as well as their body language in the current game. Face of flight or focused for the fight? Blinking rapidly tends to convey stress, anxiety, and timidity, which may indicate that the moment is too big for a coach, player, or team to handle. My son Eli and I stayed up late to watch the first game of the 2026 Western Conference Finals. The San Antonio Spurs, led by Victor Wembanyama, won a thriller in double overtime against the Oklahoma City Thunder. I told him before heading to bed, “The Thunder are going to win game two by 8 to 10 points.” OKC won by 9. The Spurs gave a valiant effort, but OKC players had a different look in their eyes compared to the first game. They picked up their defense, pushed the tempo, and rode the wave of their electric crowd to a much-needed win. As the defending NBA champs, they had no other choice but to save face.

Incentives matter more than player stats or prop lines, which sports fans or gambling enthusiasts may not realize. Let’s revisit Caris LeVert’s game four breakout performance against the Cleveland Cavaliers. In the first round of the playoffs against the Orlando Magic, he averaged under 3 points a game. LeVert is a capable player; however, he struggled mightily against the Magic. But in the second round, LeVert averaged over 9 points, a 3x per-game scoring boost compared to the first round. What happened? Here’s my take. First, LeVert used to play for the Cavs. Obviously the team traded him; he may still have beef with Cavalier ownership about this. Second, he was born in the Buckeye State but played college basketball for that team up north. Cleveland Cavs fans reacted with boos to images on the jumbo screen of Jim Harbaugh, the former head coach of that team up north. I’m sure this fired up LeVert even more. Third, he is from Central Ohio, a roughly two-hour drive from downtown Cleveland. Now why wouldn’t he play better in front of family and friends who made the trip up from Columbus to support him against his former team? I would never share, no matter the financial incentive, any information for public consumption that could lead a problem gambler into financial ruin based on my “inside-information” recommendations. Keep the millions; I’m good.

Faith Framework, Belief Continuum

The faith framework (in what someone predicts while being a voice of trust) is part of the belief continuum, from plausibility to possibility to probability. Plausible. Possible. Probable. As you can tell by the synonym and semantic wordplay used, this type of belief offers the illusion of certainty at the expense of free choice through a cleverly packaged neuroscience hacking system. Guess where the faith framework and belief continuum are located in the brain? The temporal lobe, an area that also houses long-lasting memories, deep-rooted emotions, life-application scripts, trigger-inducing sounds, and aromatic-blended scents. The fragrance of a (perceived) winning bet passes the smell test long before, not after, it ever happens. And we know expectation and experience don’t always see eye to eye! Now, this doesn’t deter most gambling addicts who get caught up in the expectation-experience disappointment zone. No, they’re still convinced of the eventual outcome (in spite of evidence to the contrary), which is why they place their unwavering faith that it, or a follow-up wager, will at some point pay off.

This is the classic case of the stick dangling the proverbial carrot, also known as Pavlovian conditioning or associative learning (where a test subject can only opt in but not opt out of a reflex-guided experiment). Yes, dopamine may drive the conviction vehicle, but depleted levels of oxytocin are what fuel a wagering addict’s willingness to stay on the gambling belongingness bus, better yet, bankruptcy bust. And this, my friends, is an exhausting ordeal to pull off. Online all the time but in need of a lifeline. In a VIP suite full of other “lucky” gamblers while feeling alone in the corner of the room as the biggest loser. With family and close friends—at festive events full of laughter—who aren’t privy to the depth of darkness and newfound space-cadet ways of their loved one drowning in misery. If you’re an empath like me, you can feel their pain and grasp how problematic this whole setup is. It’s not a fair fight when a problem gambler can’t see or duck from the next punch coming. His reflexes are compromised, just the way gambling companies and their well-paid addiction scientists like it. (As a self-taught neuroscience hack and transparency ideologue, oxytocin is a connection pathway that I often appeal to as an empathetic-driven writer. Honesty is always the best policy.)

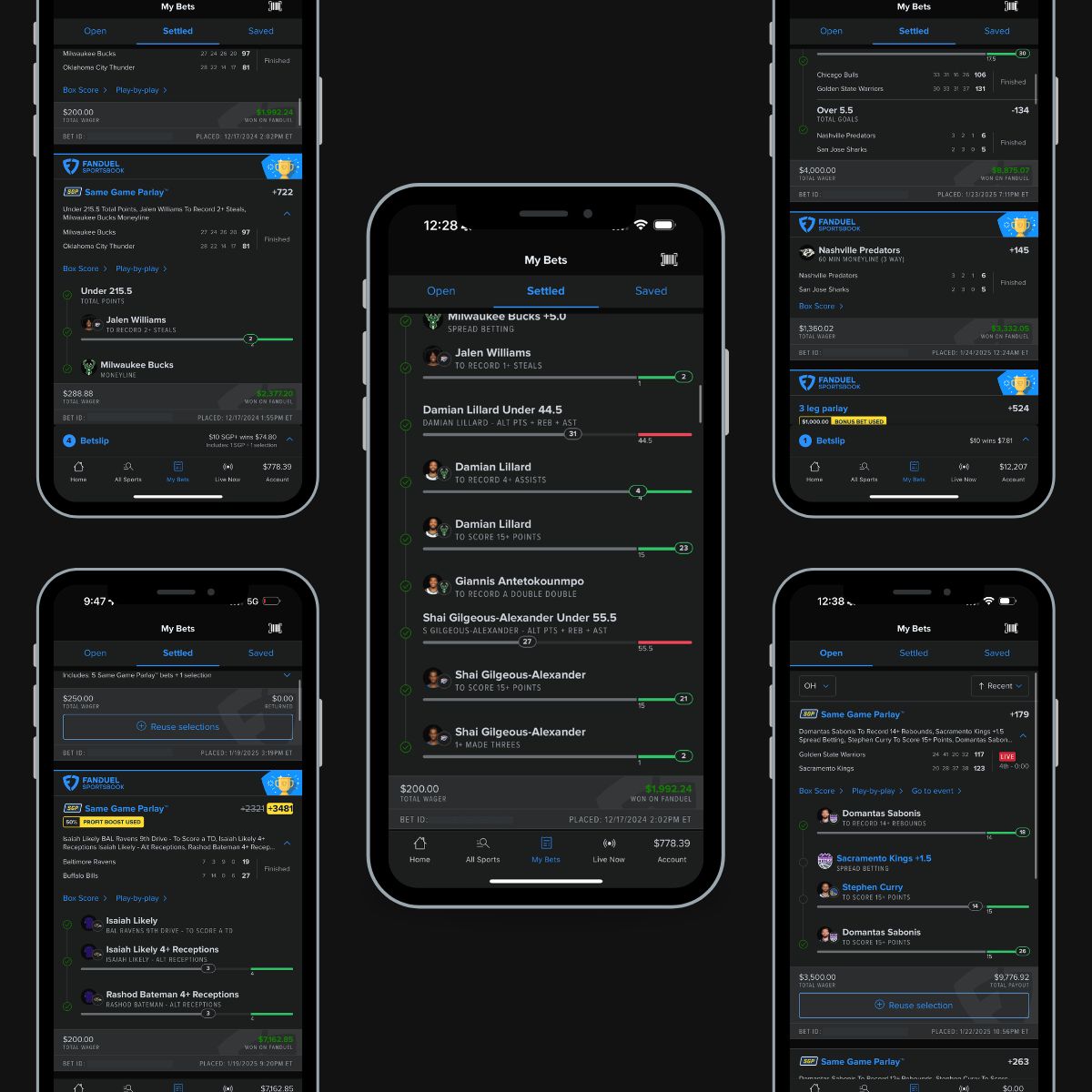

Before closing out this article, I want to introduce readers to a young man that I’ve had the pleasure of mentoring for the last year or so. To protect his identity, I’ll refer to him as “Ryan,” the alias he requested. Ryan’s a natural go-getter with an entrepreneurial spirit and stellar background in sales. His wisdom and understanding of life are quite impressive for a 24 year old. Heck, I learn just as much from him as he gleans from me. Unfortunately, Ryan’s a former sports gambling addict. At one point, his winnings exceeded $120,000. His losses? They were just over $225,000. Net-net, he’s in the hole more than $100,000. Some of his wins and losses are highlighted in the screenshots below. Ryan won early and often in the beginning, which kickstarted his gambling addiction. Off the rip, he won $28,000 in three hours without having a dollar of his own money at risk! As a result, BET365 banned him after he beat their algorithm; he won too much too quickly. However, the Midas touch eventually wears off for every above-average sports gambler, Ryan included. His addiction caught up with him, and he paid a handsome price for it—financially, relationally, and inspirationally.

A few years ago, Ryan’s sitting in the back seat of his parents car on the way to dinner with them. He notes, “I had just lost over $3,000—in a matter of minutes—using a sports betting app! Shocked and dazed, all I could do was continue scrolling while looking for my next pick-me-up bet.” The algorithm sent him into a state of fog, a common side effect experienced by problem gamblers. Ryan adds, “I couldn’t even have a meaningful conversation with my mom and dad. My mind was somewhere else, which was so disrespectful to them.” And that’s what a gambling addiction does to many players: they morph into (or take on) a scaled-down version of their best selves. It’s subtle, but as they bet and lose more, meaning is lost in lockstep with the money. Ryan continues, “I lived for that next wager. I made the erroneous assumption that this would be my purpose in life, an A-rated gambler who could consistently beat the odds.” His emotional state took a beating right alongside his betting: disgust, anger, shame, regret, and shock overwhelmed him. He concludes, “I lost myself and a girlfriend over my out-of-control gambling problem. What’s worse, I wasted so much time chasing an empty thrill.” Ryan’s still here, but some problem gamblers aren’t as fortunate. In the last installment of this series, I’ll discuss the pathological effects of runaway gambling addictions. Thank you.

Recent Articles

Gambling Addiction (Part I)

Huge risks, big(ger) payoffs. For the record, I’m not a gambler. Nope, it has never been a gravitational pull of mine. However, I have seen many people, including former NBA teammates, get bitten by the gambling bug over the years. The side effects? Well, they’re dose dependent and ever present. More on them a bit later. Gambling has always been a part of the NBA culture, whether it’s card games with multi-thousand dollar jackpots on long road trips to the east (or west) coast in private planes, frivolous bets on half-court trick shots before and after practice, or locker room wagers on which referees are likely to officiate hotly contested playoff games, from one round to the next. I witnessed these scenarios—and many others—firsthand in the NBA. “Bet that” was part of our everyday, testosterone-driven lexicon; nothing was off the gambling table. It’s much worse today! The side effects of gambling addictions result in long-lasting symptoms, from financial problems to relationship challenges to internal stressors to sleepless nights to mental health issues, in particular, circadian rhythm disruptions. By the way, May is Mental Health Awareness Month. And yes, even casual betting indulgences can morph into full-blown gambling pursuits when triggered by an unforeseen setback, such as a job loss, economic downturn, death of a life partner (or beloved family member), or any number of crises-related events. What usually happens here is the chase becomes the run to the fun. To a place of refuge or from a space of torment. Either way, the addiction fix is in.

Are some individuals, like myself, predisposed to addictive tendencies because of genetic (or heritable) traits, epigenetic (or environmental) influences, or optogenetic (or shiny-object) sources? The evidence is mixed. Opinions vary in the medical community from “not at all” to “significantly so.” Here’s what we do know about people who have an innate ability to bet on themselves, many gambling addicts included. These individuals generally fall into one or more categories: movers and shakers, risk takers, and/or opportunity makers. Let’s break each of these down from a psychological point of view:

Movers and Shakers

Movers and shakers make things happen. Right now! For them, sitting still is missing out on the action. Even in a confined space of intense boredom, their mind is moving from one thought to the next. Broadly speaking, they’re long on creating million-dollar ideas in record time but short on producing the feasibility studies needed to pull them off. The number one drawback of movers and shakers? It’s easy for them to confuse movement for progress. In fact, going somewhere may not get them anywhere.

Risk Takers

Next up is risk takers, who cover the gamut. At one end of the spectrum are methodical and meticulous risk-taking brain types. Planning typically comes before acting. They’re philosophical and are often described as having “mundane personalities.” They usually excel in math and sciences, which is why they’re drawn to analytics and arbitrage strategies when gambling. At the other end of the risk-taking spectrum, we find carefree and careless brain types. When they feel it—that urge to splurge or need for speed—they’ve already acted upon it. An impulsive purchase. An unsolicited critique. A high-stakes wager. For these individuals, they assume delay automatically means denial. And in the world of sports betting, they’re prone to losing their shirts. Literally! Due to their spontaneous and combustible personalities, they’ll jump in the pool at the casino after a big win or pledge their home as collateral to chase a huge loss. One thing is fairly certain: they often move in lockstep with their mood. (I’ll cover this phenomenon in greater detail in Part II of this series.)

Opportunity Makers

Opportunity makers do just that … make opportunities happen for themselves and others. With this group, where there’s a will, there’s a way. Gut instincts, not impulses, drive their opportunity bus. As hockey legend Wayne Gretzky once said, “You miss 100 percent of the shots that you don’t take.” So true, but some shots are not worth taking regardless of the colorful appearances, celebrity endorsements, or commercial advertisements. Why gamble with your health or wealth using somebody else’s opinion?

Why Males Can Compartmentalize Gambling Losses at the Expense of Isolated Wins

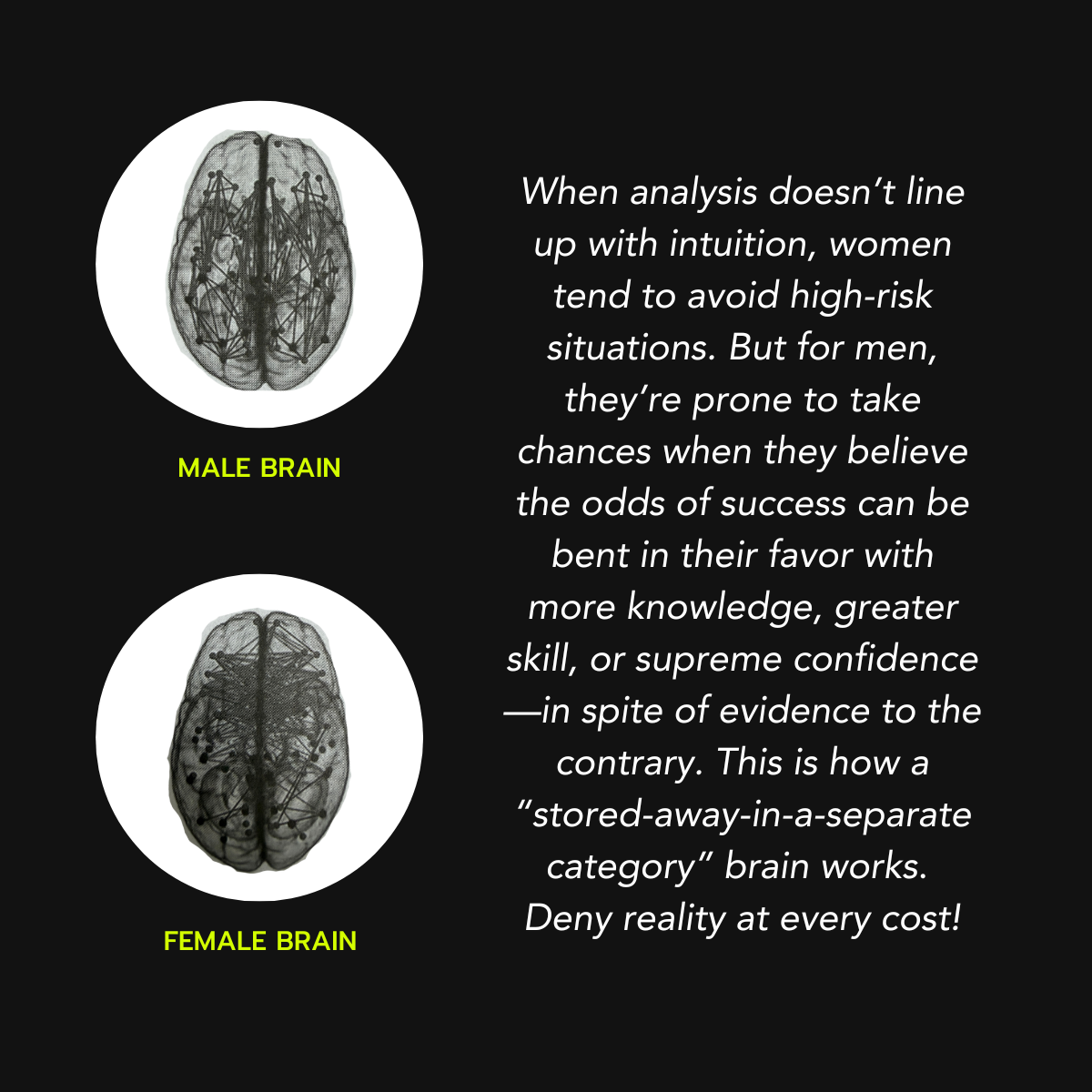

Not surprisingly, males are more impacted by gambling addictions than females. By a wide margin! Sounds controversial, but it shouldn’t be. According to Dr. Helena Boschi, an accomplished author and renowned psychologist specializing in applied neuroscience, she writes, “Men’s brains display front-to-back connectivity within the [left and right] hemispheres, moving between perception and decision-making” (reference #1). Women’s brains, Boschi notes, “are wired more laterally, between the hemispheres, suggesting greater communication between analysis and intuition.” (reference #2). Fellas, don’t shoot the messenger, but women are generally more intelligent than men. Ladies, I’m sure you already know this :). Neuroanatomy differences may also explain why male drivers pay higher car insurance premiums than female motorists. If male and female brains are exactly the same, then why are our risk profiles for automobile insurance so vastly different? Independent of ADD and ADHD diagnoses, risk-seeking behaviors are usually par for the course in the male brain. And gaming companies know this, which is why pubescent boys are being set up to become lifelong gaming and gambling customers through addictive video games with picturesque backdrops, exhilarating sounds, and masculine messages. Optical illusions. Acoustic frequencies. Semantic associations. A marketing campaign trifecta with terrible societal consequences.

Reference #1 and #2

Dr. Helena Boschi. Why We Do What We Do: Understanding Our Brain to Get the Best Out of Ourselves and Others. Chapter One, page 15. Wiley Publishing, 2020.

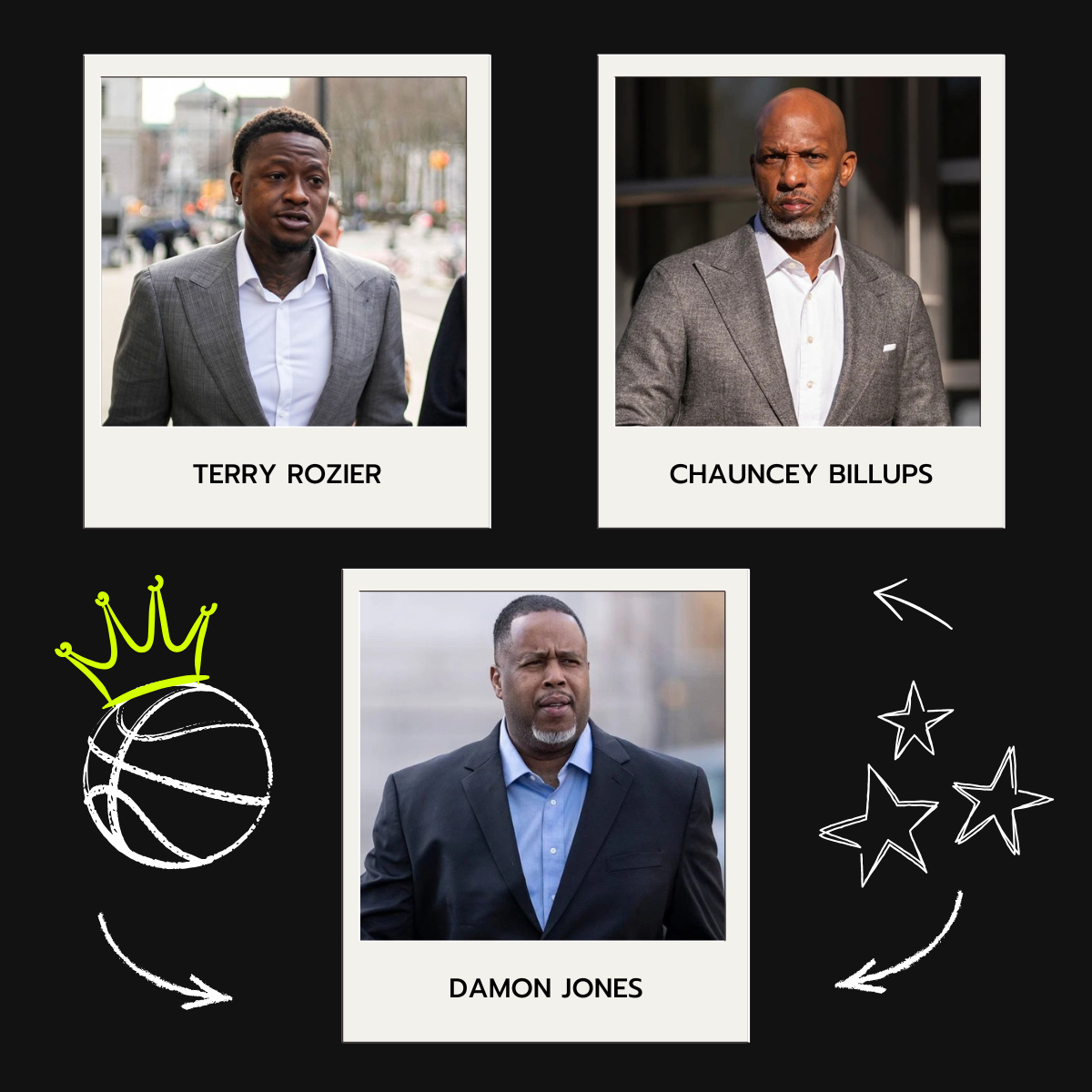

Chris Broussard is a sports analyst and commentator on FS1. Alongside Nick Wright, he is the co-host of the popular afternoon sports show, First Things First. A devout Christian, family man, and community ambassador, Broussard has worked for The New York Times, ESPN, ABC, and Fox Sports Radio. He covered the NBA’s blockbuster gambling scandal in 2025 involving Terry Rozier, Chauncey Billups, and Damon Jones. Rozier, a guard with the Miami Heat, and Billups, an NBA Champion and Portland Trail Blazers head coach, have been placed on indefinite suspension by the league as their cases are still under FBI investigation. Jones, a former NBA player and teammate of mine in Sacramento, pleaded guilty on April 24, 2026, to two counts of wire fraud conspiracy. In an interview, Broussard highlights, “The professional leagues may have inadvertently made a deal with the devil by getting in bed with these gambling companies.” He adds, “And there was no way to shield players from getting caught up in some kind of gambling scandal.”

I was heartbroken by the news when it first broke. I thought to myself, “This is a really bad nightmare. Current and former NBA players allegedly mixing and mingling with mob families to dupe unsuspecting poker players out of millions of dollars through rigged setups. Say it ain’t so?” The game I love and league I defend is facing a crisis in confidence on three fronts. First, this scandal will fuel skeptics who already think (with this serving as added proof) that the NBA is nothing more than scripted choreography. It’s not, but every missed open shot, careless turnover, or senseless foul will be scrupulously examined from a “suspect-entertainment lens.” Second, current players will face even more scrutiny from sports betters masquerading as diehard fans when wagers miss the payoff mark. An irate sports bettor rolled down his car window to confront NBA superstar, Jimmy Butler, who was standing on the curb in New Orleans while in town to play the Pelicans. “Bro, I put $3,000 to win 30 [thousand]. Why you ain’t have 30 points? Jimmy Butler, why you didn’t have the 30 points? You were supposed to go OVER b—h. You work for Vegas? You work for Vegas?” Third, how will America’s youth be affected, really infected, by the gambling bug if no safeguards are put in place to protect them? Without an alternative course of action, they’ll likely fall victim to gambling devices in adulthood, if not before. We’re in big trouble folks.

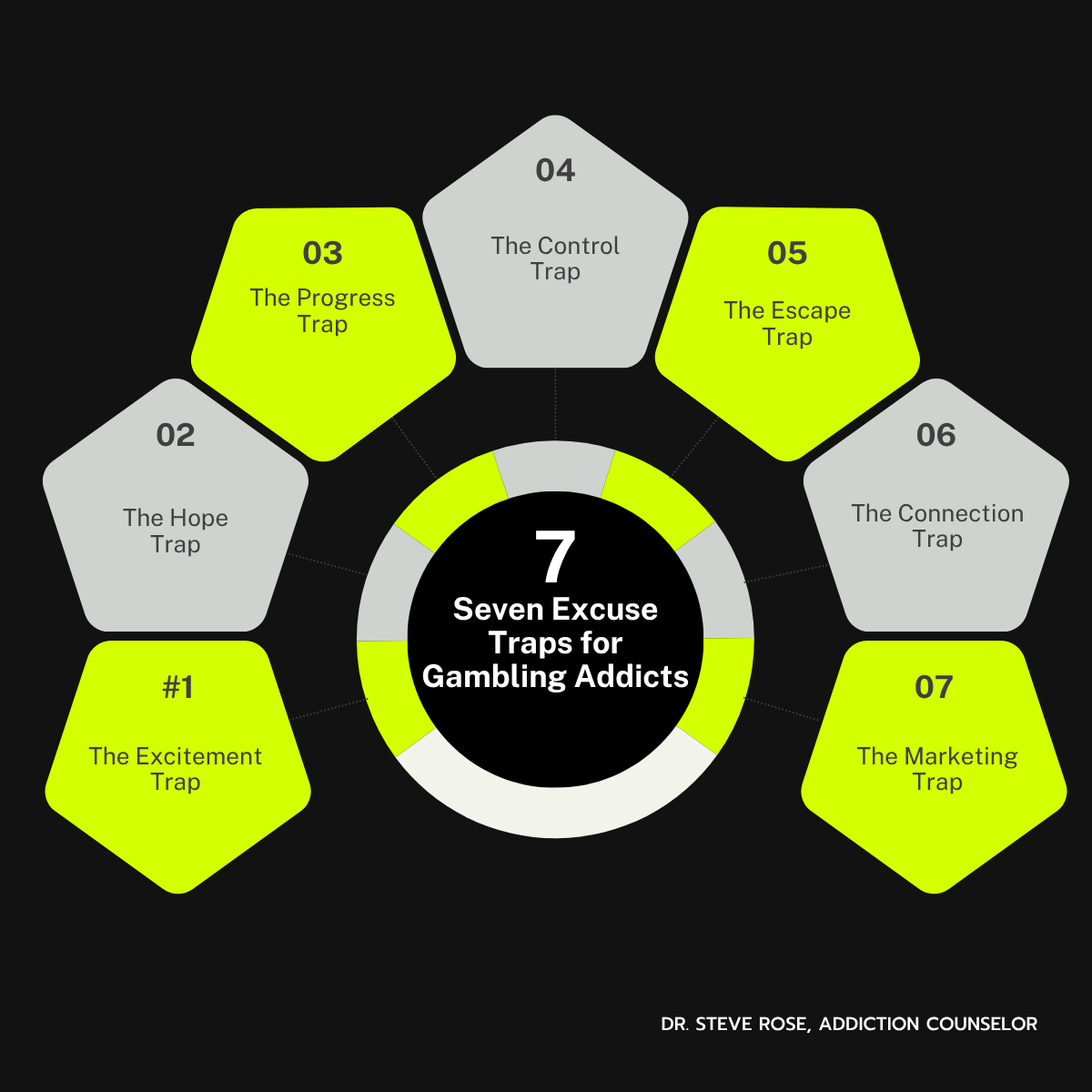

In closing, I shared the stage recently in Denver with Rob Minnick, a former gambling addict now turned recovery advocate. We were participating in an event hosted by Doura-Schawohl Consulting and several Colorado legislators to limit sports betting in the state. (The bipartisan bill passed this week and is awaiting Governor Jared Polis’ signature.) For six years, Minnick struggled with a runaway gambling addiction. From parlays to blackjack to slot machines, he gambled every day online and in the casinos for 6 to 8 hours. Upon first glance, he didn’t fit my jaded, gambling addict profile. Minnick is polite, soft-spoken, and measured with his words. His Youtube channel and One Day At A Time (ODAAT) website are timely resources that shed light on this growing epidemic, with over six million Americans battling mild to severe gambling addictions (reference #3). Minnick’s story is best illustrated against the backdrop of Dr. Steve Rose’s Seven Excuse Traps.

Reference #3

Dr. Kent S. Hoffman. Addiction Help: Gambling Addiction Statistics. March 3, 2026. www.addictionhelp.com/gambling/statistics/

With Excuse #1: The Excitement Trap, Minnick’s addiction was set in motion by that initial dopamine hit coursing through his body. He points out, “This is where I got suckered in by the fun. Without that thrill, the gambling ride would have been boring and pointless for me.” The dangling carrot, Excuse #2: The Hope Trap, kept Minnick in the gambling feedback loop. Pay up. Play on. Pray for. That next win streak! Even when his losses piled up, Minnick convinced himself that one more bet—a winning wager—would cure his addiction in full. He admits, “Gambling addicts dig in when they should bail out.” That ray of hope, a promising payday, kept the hype fuel lit. The Progress Trap, Excuse #3, is where gamblers find themselves stuck in a rut with no tow truck in sight. Minnick warns, “Here is where the near-miss fallacy kicks in. You lose by a point and tell yourself, ‘Man, I was so close. Keep going.’” A gambling addict’s brain releases a larger dose of dopamine in comparison to someone in the general population who also almost wins. That extra surge fed Minnick’s urge.

Excuses 4 and 5 can be paired together, The Control Trap and The Escape Trap. Discipline, due diligence, and determination were factors that allowed Minnick to feel in control in an uncontrollable environment. He even developed some peculiar rituals while trying to escape from the madness. “I wore the same clothes, sat in the same spot, and hit the blackjack table in the same place every time before I bet. I even listened to vedic chants to center myself. Of course, nothing worked.” Excuse #6: The Connection Trap is where gambling delusions reach their highest peak. Minnick shares, “You’re paying for friendships with complete strangers.” He adds, “Your losses are funding the luxury suites gambling companies invite you to enjoy. Think about how crazy that is!” What’s even more disheartening is that VIP gamblers tell themselves, “I belong here and can get pretty good at this.” And just when a gambling addict tries to get out, the push notifications and free-cash ads ramp up. That’s why Excuse #7: The Marketing Trap, won’t let a betting enthusiast just walk away on his or her own terms. Minnick explains, “It’s so sinister what gambling companies do; they know us almost better than we know ourselves.” He concludes, “Fighting fair is not in their best interest financially.” Stay tuned for Part II in this series, The Physiology of Gambling Addictions, which will be released next week.

Recent Articles

Economic Empowerment - Part Three

Financial Literacy vs. Economic Empowerment (Part Three)

It's Not a Fair Fight!

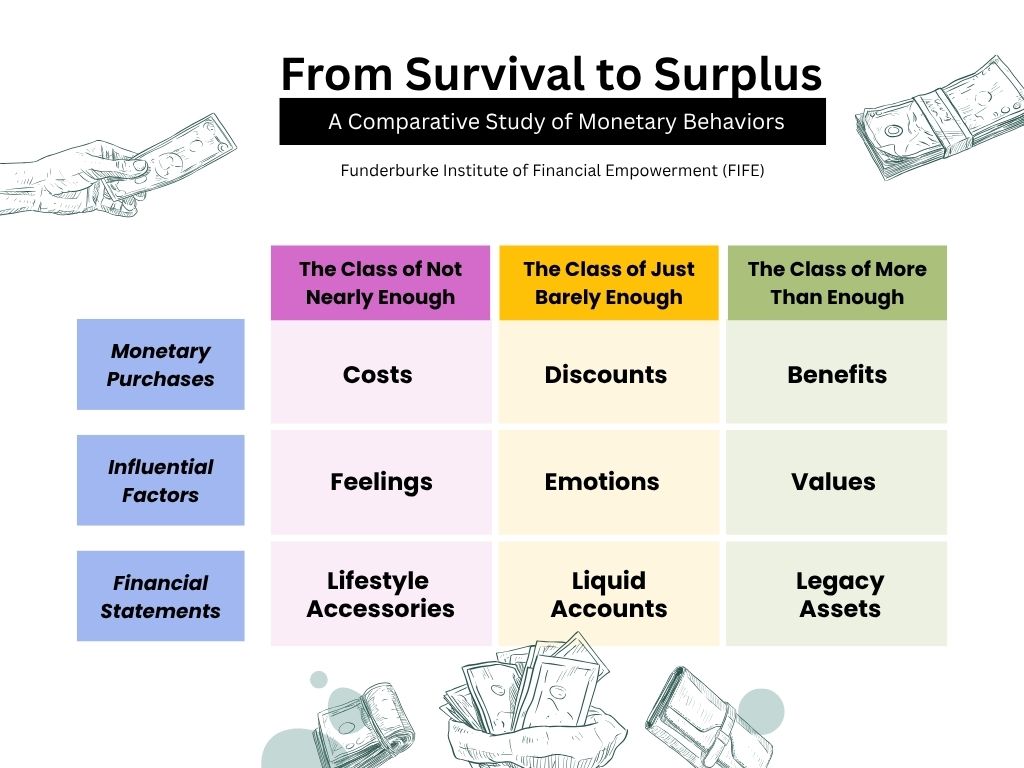

Costs. Discounts. Benefits. Feelings. Emotions. Values. Lifestyle Accessories. Liquid Accounts. Legacy Assets. When it comes to money, how you—or anyone else—use it speaks volumes about your financial mindset and class affiliation. In this third and final installment of the series, we’ll examine how social classes think, act, and behave economically in America and likely around the world. “Thinking” has everything to do with one’s thought process in dealing with money. “Acting” highlights how a person, couple, or family performs in handling financial matters, from calmness to anxiousness to ostentatiousness to unpretentiousness (and everything in between). “Behaving” underlies the ingrained habits, or default choices, that people make when allocating financial resources each month. One last point in this opening paragraph, and I’m paraphrasing a quote I heard one of my mentees share: Our financial frequently has everything to do with our economic frequency. And even if this is out of tune, we still march to the beat of its dictates anyway. I wrote about this phenomenon, and over 50 other social class comparisons, almost a decade ago in my book, Sociopsychonomics.

The Class of Not Nearly Enough

First up is the class of economic hardship, or those who’ve been dealt (often through no fault of their own) a bad financial hand in life. What’s so fascinating about working with groups on the fringes of society—which was my reality for nearly two decades—is that they tend to prioritize feelings over values, costs over benefits, lifestyles over legacies. It’s nearly impossible to break free from the shackles of economic bondage when instincts and impulses drive spending decisions. This is especially problematic when the pain and pressure of a brutal existence, coupled with inherited trauma, compels marginalized communities to live in, and only for, the present moment. Their response economically? Spend money, no matter the costs, on shoes, clothes, and other “outward” accessories to uplift their “inward” spirits. The problem? Debts accumulate on the liability side of the balance sheet, notably credit card charges and payday loan advances with every depreciating asset purchased. And so the vicious cycle of poverty continues, from one generation to the next.

The Class of Just Barely Enough

Property taxes have outpaced salary gains over the last several years. Grocery prices have continued to rise, even when supply has surpassed demand. Thanks to the law of diminishing returns, angst is in the air as blue-collar workers struggle to make ends meet—too few dollars to satisfy too many bills. They are stretched thin personally, professionally, and psychologically while trying to fund their middle-income lifestyle. Savings are being depleted. Job layoffs are starting to pile up. Doubts are drowning out the dreams of earning their fair share of the American pie. Fairness is not on the side of those who are caught in the crosshairs of having just barely enough. And their admirable work ethic, AWE for short, isn’t the leveraging tool that it once was in decades past. Employer-provided defined benefit plans (aka pensions) are all but gone; for the most part, they’ve been replaced by defined contribution plans (where the onus is now on employees to manage their own retirement accounts, in particular, risk-and-return tradeoffs in lieu of performance outcomes). Unlike the poor, there’s no social safety net for the middle class. Nope. But they do have a time sensitive, binary choice to make: get pushed down to the economic-hardship class, or move up to the appreciating-asset class. Tick tock.

The Class of More Than Enough

The good news is that the affluent class has added thousands of American households to this social strata of privilege over the last two decades. The bad news? Millions more are needed right now to close the wealth gaps in our country. Affluent-positioned Americans (APAs) place a premium on noteworthy benefits, value-driven principles, and legacy assets in accordance with their heritage script. Truth be told, this multilayered approach works for several reasons. First, they understand that the benefits received from a given product or service are worth the expense(s) made. Money is one thing, meaning is altogether different. Most APAs are purposeful in everything they do, including how they allocate financial resources; they don’t leave anything up for chance. Their world of investing is not confined just to certificate of deposits (CDs), stocks, bonds, mutual funds, and alternative investments. To them, getting a good deal isn’t about cost or a discount. It’s about their developmental advantages—what they gain, how they improve, where they excel, who they (or their children) become, and why they win. Time after time in their life and livelihood pursuits!

Second, values are the guiding principles that shape daily decisions, actions, and activities. Here’s the kicker: These tenets should be non-negotiable, regardless of one’s social class. If they aren’t, then they can’t be classified as values. Guiding principles serve many purposes, but chief among them is helping the wealthy avoid mission drift. As boundary markers and benchmark makers, values keep APAs in play when other social classes lose their way. Economic downtown? Stay the course. Political upheaval? Keep moving forward. Death in the family? Grieve as needed but stick to the written script. Third, legacy is arguably the most important component of the affluent-class playbook. Now, every individual or family leaves behind a legacy, but not every legacy is worth leaving behind. Sounds harsh, I know. But if an individual, couple, or family gets this wrong, benefits and values won’t matter. Why? Because there’s nothing to pass on to the next generation. No game plan. No goodwill. No great name. I pray that this three-part series has been a blessing to you. To our LFYO supporters and business partners, thank you for your generosity and hospitality in helping us equip and empower the least among us here in Central Ohio.

Exciting News!

Coming Next Week!

Stay tuned for our upcoming 2026 Fundraising Luncheon announcement, where we will unveil this year’s keynote speaker and host location.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us for our annual fundraiser! We’re passionate about equipping the next generation with the tools they need to go from just 'knowing' about money to truly mastering their economic future.

Related Articles

Economic Empowerment - Part Two

Financial Literacy vs. Economic Empowerment (Part Two)

It's Not a Fair Fight!

Start the course in childhood, continue the journey throughout adulthood. Developing financial life skills within the framework of wealth-building initiatives—investing in stocks, bonds, mutual funds, and other compounding-growth options—are critical to helping at-risk youth connect the academic and opportunistic dots. Yes, these concepts are foreign to most fifth-grade students (regardless of their family’s economic situation). But an introduction to personal finance should come sooner rather than later for children from under-resourced households. They’re quite familiar with the typical, outdated motivational track: Go to school. Secure a job. Earn an income. With some minor revising and major revealing, vulnerable students should have access to this updated, twenty-first century educational template: gain a foundational understanding of wealth-building principles in elementary school; identify talents, gifts, and abilities in middle school that align with a child’s mission-driven fit; and create a pathway for high schoolers to become philanthropic contributors as change-agent specialists within their respective communities. When high-need students experience the miscues of financial mismanagement and the virtues of wealth accumulation firsthand in game-based settings, they’re generally more aware and excited about their future prospects and place in this world.

Not Nearly Enough vs. Just Barely Enough vs. More Than Enough

One of the biggest mistakes middle-class facilitators in the financial literacy field or educational arena make when working with low-income households is this: They often place limits on how far up the economic ladder the less fortunate (as well as members of their own social class clique) can climb. Surface-level mantras, even innocent ones, do more harm than good. “Get a safe and secure job.” “Stick to a realistic budget.” “Be careful investing; it’s not that much different than gambling.” You get the picture. Safe and secure jobs don’t exist anymore in our modern, AI- and algorithm-driven world. Workforce cracks, aka seismic shifts in the (un)employment landscape, are just around the corner. Budgeting is so passé, so why not highlight cash flow management instead? The former is suffocating, while the latter is liberating. Yes, semantics matter a great deal when financial freedom is on the line. True enough, speculative investing is akin to gambling. However, calculated risk taking—when guided by and guarded with due diligence—is not. As any value investor knows who typically pays more attention to balance sheets than income statements (when evaluating prospective companies), extensive research is the key to finding good stocks selling at a steep discount to their intrinsic value or fundamental worth.

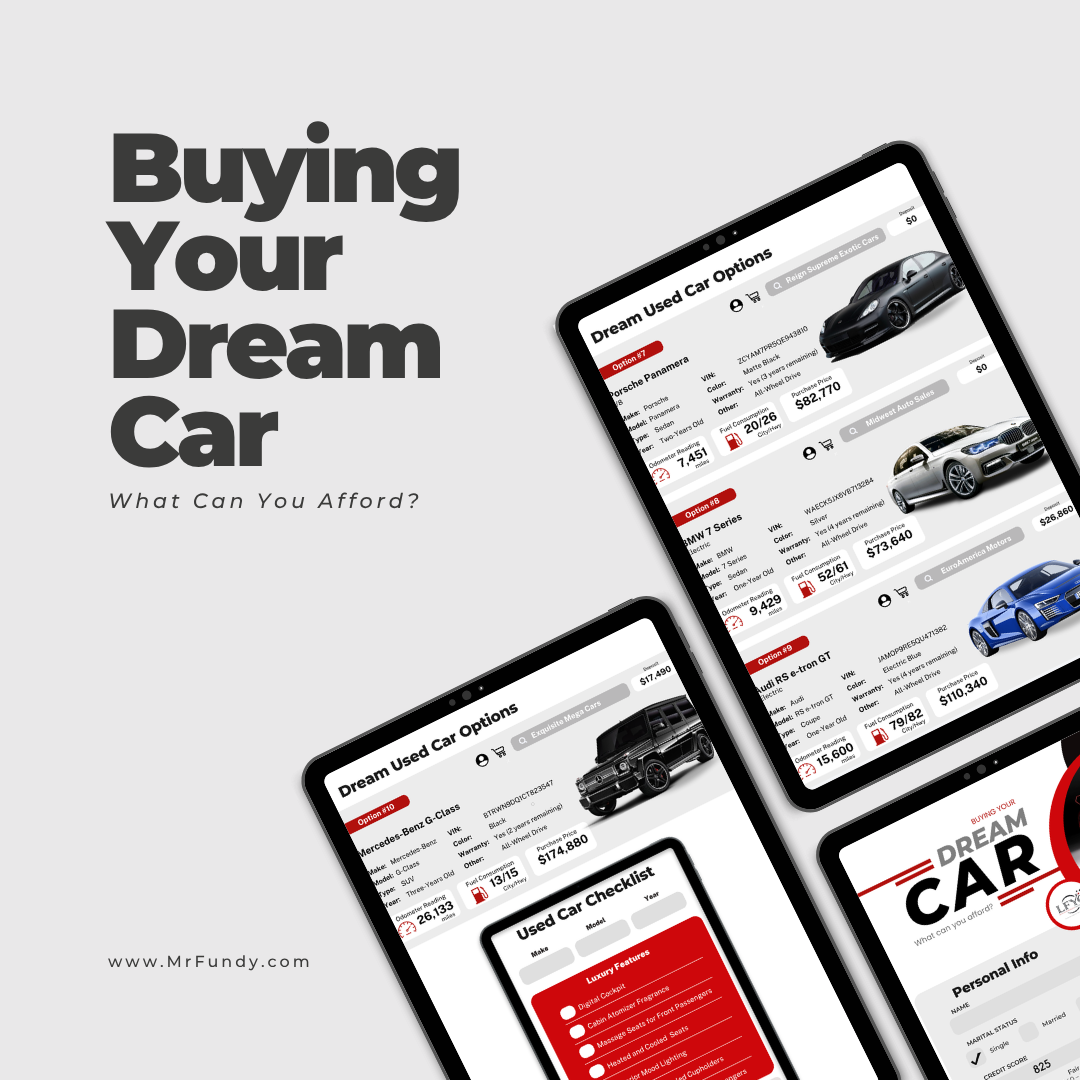

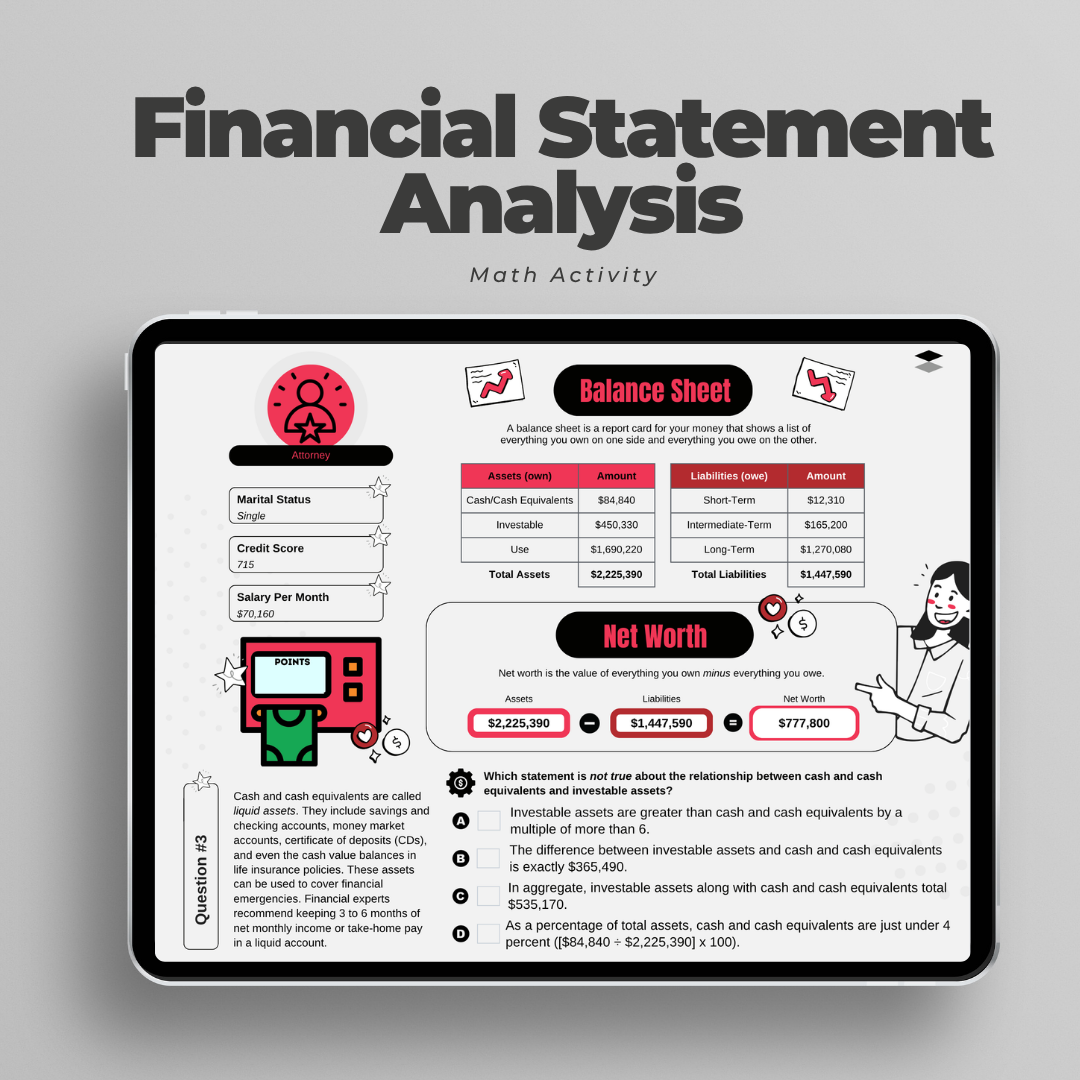

In settings using make-believe money, vulnerable students should dream big. In our Buying Your Dream Car activity, we allow underserved youth to reach for the stars. In this interactive exercise using an iPad, students are assigned a hypothetical occupation, monthly salary, marital status, credit score, and balance sheet to purchase their dream car. The experience even includes step-by-step instructions on financing considerations, notably making a down payment or placing a deposit, buying an extended warranty, and selecting the number of monthly payments until the bank loan is repaid. Luxury vehicle selections are as follows: Range Rover Sport, Mercedes-Benz Maybach, Bentley Flying Spur, Ferrari Spider, Lamborghini Urus, Tesla X, Porsche Panamera, BMW 7 Series, Audi RS e-tron GT, and a Mercedes-Benz G Wagon. While scrolling through the list of dream cars, the collective oohs and aahs of students is music to our ears. The acoustics and optics in the classroom are why we, Monya and I, do what we do as economic empowerment crusaders. Create an enriching environment—through gamification activities—that places each student in the driver’s seat of holistic success. As tour-guide representatives, it’s incumbent upon us (like teachers, principals, and administrators) to provide inner-city youth with the navigational aptitude needed to achieve a prosperous life with legacy benefits.

In closing, choice architecture (along with consequence assessment) is the name of the life improvement game for at-risk communities, who often choose the path of least resistance when they can’t opt out of higher-level thinking while evaluating mentally challenging strategies. Here’s what I’ve learned as a non-traditional educator and certified financial planner over the last 15 years: Data processing can quickly turn into information overload for vulnerable students who are short on academic conditioning. And when fatigue sets in, disinterest levels ramp up. The remedy? Provide a constant supply of stimulating flashpoints that connect inner-city students’ present reality (personal boredom) with their future possibility (financial freedom). A well-timed break to serve healthy snacks helps too! You see, the dream car they desire to purchase down the road comes with a hefty price tag. Whether it’s a car, house, or stock investment, everything has a cost. Pay now, play later. Play now, pay later. That choice, even by default, is theirs to make—whether they realize it or not. And reminding LFYO participants what could be and how they can achieve it is rooted in biochemical tuning. “Pay-careful-attention” comments boost norepinephrine or concentration levels. “Imagine-what-life-will-be-like-when-you’re-net-worth-is-off-the-charts” reflections increase serotonin or feel-good levels. “Stay-with-it” promptings amplify their endorphin or resiliency levels. Without question, neurotransmitter development is the most important factor in helping inner-city students step outside their math sweet spot and into their computational growth zone through personal finance concepts. And friction is required for this to occur! We have included a page from one of our financial math worksheets below for your review. Keep an eye out for part three in this economic empowerment series, which I’ll release next week. Until then, stay blessed.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us for our annual fundraiser! We’re passionate about equipping the next generation with the tools they need to go from just 'knowing' about money to truly mastering their economic future.

Related Articles

Economic Empowerment - Part One

Financial Literacy vs. Economic Empowerment (Part One)

It's Not a Fair Fight!

Financial literacy is incriminating, highlighting where people fall short in the area of basic, money management habits. But economic empowerment is liberating, showcasing who they can become as wealth-building accumulators and legacy-minded progenitors.

April is National Financial Literacy Month. Great optics, lackluster semantics. Translation: Placing a monthlong spotlight on helping Americans develop better financial habits is definitely needed. However, equipping them with the mindset and skillset to build wealth is absolutely necessary. Here’s why. The state of wealth among racial groups, which the Covid pandemic exacerbated, should be our collective wake-up call. Black and brown communities are way behind financially. According to the Pew Research Center, the median net worth of African Americans in 2025 was $44,100. For Hispanics, their balance sheet was slightly stronger at $62,000. The net worth of white households was around $250,400, almost six times higher than their African-American counterparts. In comparison to Asian Americans, the wealth picture is even bleaker for black and brown families. Asian Americans have a median net worth of $535,400, 12 times greater than African Americans and roughly nine times more than Hispanic Americans.

This disparity in wealth is quite troubling on several fronts. First, children from asset-deprived households often see their economic world from a glass half-empty perspective. Second, this life outlook can, and usually does, lead to self-defeating attitudes and self-sabotaging behaviors that result in self-fulfilling prophecies guided by this pessimistic belief system: “Fate is not on our side; we can never bend the odds of financial success in our favor!” Third, fatalism inevitably pulls high-need communities toward gambling traps and lottery pitfalls—or other get-rich quick, desperation schemes—to cover the shortfall. These speculative outlets, which are often fueled by superstitious hunches and “lucky break” mantras, end up causing more financial pain than they alleviate. That’s why LFYO offers a downstream playbook to deal with this upstream problem across the age spectrum.

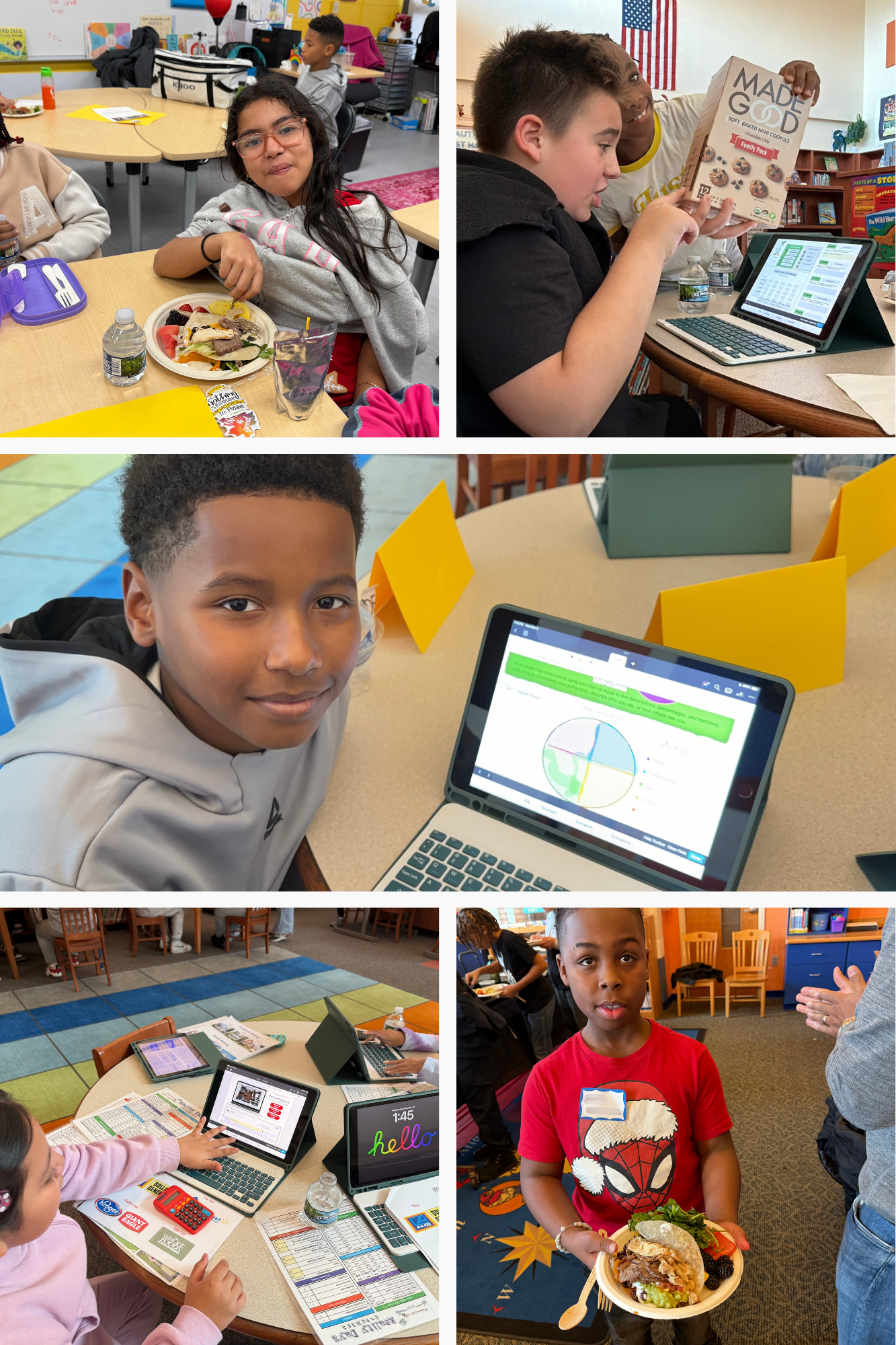

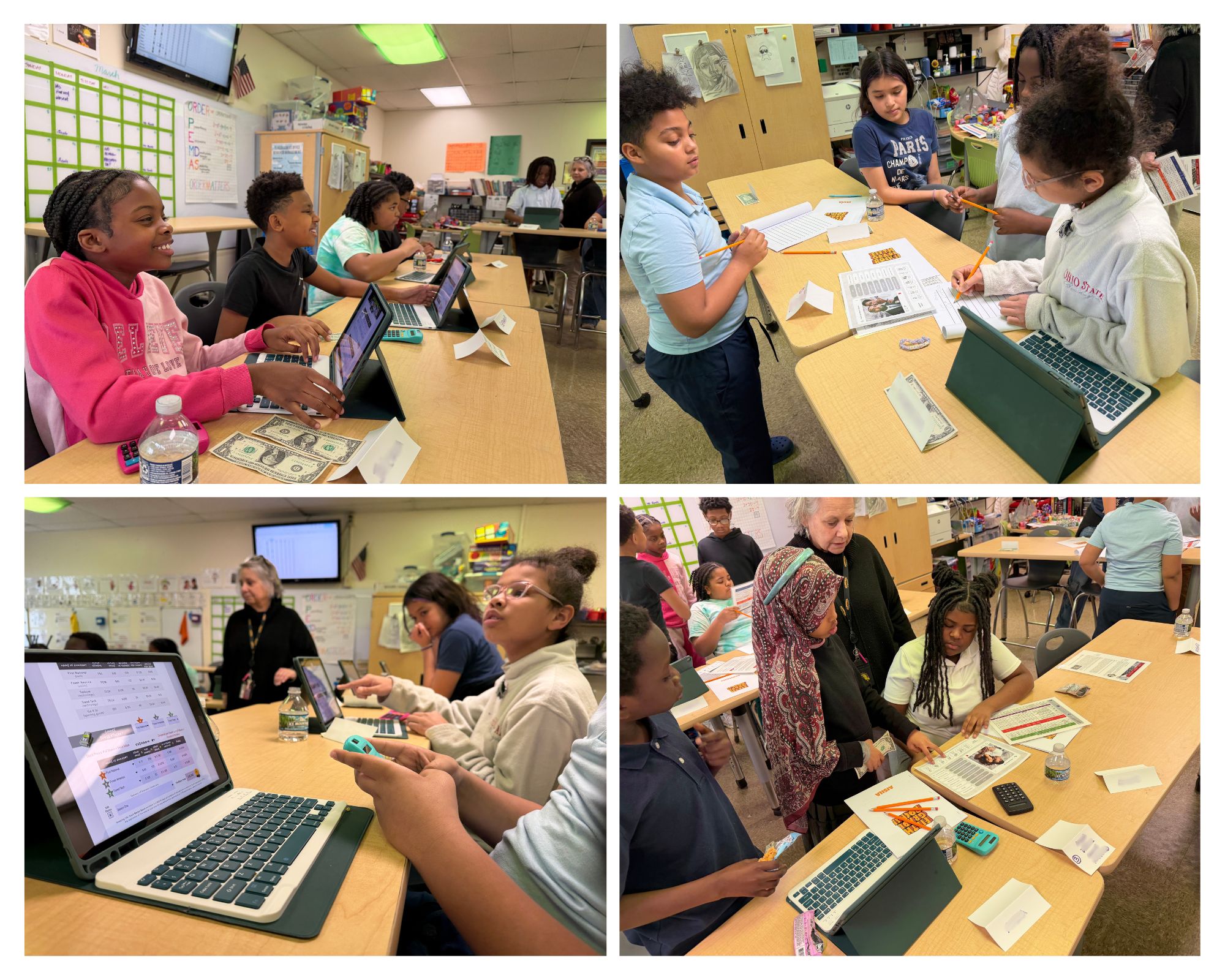

In our Investing 101 app-based game, we teach fifth-grade students who attend inner-city schools the basics of asset allocation, stock market investing in particular. (Asset allocation is the process of spreading investment funds among various risk-and-reward options, such as savings and checking accounts, certificate of deposits, stocks, bonds, mutual funds, and nontraditional offerings.) After a brief discussion on the risk-and-return profile of several mainstream investment categories, students test their skills as newbie investors. We keep things simple in this introductory game; only five options are available. One bank stock. One utility stock. Two technology stocks. One sporting goods stock. Participants select three out of the five for their $15,000 portfolio, or $5,000 for each selection. I ask the class, “Are you ready to make some real money with your knowledge?” I then follow up with, “Can you name a publicly traded bank or financial institution?” Hands immediately shoot up in the air, and each correct answer is rewarded with a dollar. “Huntington Bank.” “Chase Bank.” “Bank of America.” “Fifth Third Bank.” “Key Bank.” The same question is asked about utility, technology, and sporting goods stocks. I close out the investing session with this statement, “You can make money in an up, down, or sideways stock market.” Lesson learned by the fifth graders; the down payment to get them fired up about their financial future has been made. Here’s a fact that is rarely considered by residents in low-income communities: They walk inside or drive past the brands of publicly traded companies everyday without even realizing it—shopping malls, grocery stores, and gas stations, to name just a few. Thus, wealth-building opportunities are hidden in plain sight from them. As U.S. congresswoman Joyce Beatty pointed out to me over a decade ago, “Black and brown Americans can’t just be on the customer side of the cash-register equation. They also need to be on the owner and investor side, too!” Great advice.

Recently, we facilitated a classroom simulation with fifth graders, where each team served as financial planners by committee for five hypothetical clients, three couples and two individuals. Students provided their investment recommendations (in the form of asset allocation strategies) for clients based on risk tolerance (conservative, moderate, or aggressive), time horizon (or when a client plans on withdrawing income from the portfolio), and estimated annual return on investment (ROI) projections. From low- to high-risk selections, investment options were as follows: savings and checking accounts, money market accounts, certificate of deposits (CDs), government and corporate bonds, mutual funds, value and growth stocks, real estate properties, hedge funds, private equities, precious metals, and crypto currencies. In terms of suitability, investment options were aligned with each client’s risk tolerance ahead of time, but the fifth graders did have the liberty to allocate the $1,000,000 as they chose. Their math challenge? Make sure the numbers, fractions, and percentages correctly added up when presenting their recommendations in front of the class. Sounds like a lesson too big for eleven-year olds from disadvantaged backgrounds to handle. Nothing could be further from the truth. In fact, they even exceeded our loftiest expectations during their presentations, which is why members on the winning team each won $20. Stay tuned for Part II in this economic empowerment series.

2026 LFYO Fundraising Luncheon

September 18, 2026

Join us at our annual fundraiser as we equip the next generation with the tools to transition from financial literacy to true economic power.

LFYO's 2025 Year In Review

LFYO's 2025 Year in Review

What We Accomplished, How We Operate, and Who Supports Us

From mentoring programs at Columbus City Schools to financial life skills summer camps to empowerment-based workshops for high-need communities, LFYO impacted the lives and legacies of over 800 Central Ohioans in 2025. Our template for success is quite straightforward: place at-risk populations in “simulated” learning environments where they can experience — up close and personal — their future today. No cap! Through a partnership with the Funderburke Institute of Financial Empowerment (FIFE), my wife Monya and I have created more than 50 apps that make learning fun, automatic, and unforgettable for participants while using an iPad that we provide. Here’s why this playbook is effective on three fronts to transform the life prospects and legacy pathways of disadvantaged communities.

First, we take them up to a better place before we transport them out of a bitter space. With an emotional safety net firmly below to ease their fears on the way up! You see, poverty’s clutches are debilitating because the optics are incredibly painful while being stuck and stranded inside the economic matrix. Broken homes. Blighted buildings. Bottled-up dreams. Yep, boxed in with no way out. The remedy? Paint a beautiful portrait of what could be in an exciting, game-based setting that amplifies participants’ visuospatial framework and navigational aptitude. With the right motivational incentives and personal investments, their possibility filter is bound to improve.

Second, we help vulnerable youth and young adults upgrade their semantic (or internal-dialogue) skills. Words matter — a lot. This may seem trivial to those firmly entrenched in the successful class, but assisting fourth- and fifth-grade students from inner-city backgrounds with their word choice can literally reroute their world course. For the better! “Cannot” turns into “already done.” “Give up” turns into “keep going.” “Too hard” turns into “super easy.” Their newfound belief provides immediate relief. Why? Because a competent heart produces a confident mouth. What an awe-inspiring transformation to behold as facilitators and cheerleaders.

Third, we hold at-risk communities accountable for the growth gains they achieve from one session to the next. Or as my good friend Gerry Hammond often says, “To be counted on, one must first be accounted for.” In empowerment parlance, Hammond’s quote carries a hefty price tag for those on the receiving end of a “free” service: whenever you’re given life-transforming information (in a workbook, through a program, or from a mentor), you’re responsible for the instructions that follow. And the participants we have the privilege of serving can’t ever say, “We were never taught or shown a better way.”

Wrapping Up 2025!

Thank you LFYO supporters, corporate partners, and Coach Jim Tressel! Please click the link below to check out highlights from our amazing 2025 fundraising luncheon at Hyde Park Prime Steakhouse. Blessings to you and your loved ones in 2026.

The Business of Community Investment

A Tribute to LFYO's 40 Business Partners

Brace yourself. If you don’t like personal and professional call-outs, really call-ups, then reading this article might set off your discomfort alarm bells. So be it, because our most vulnerable youth are in big trouble and they don’t even know it. That’s why we (you and I) need to do more. A whole lot more — right now! Writing checks to or volunteering at a local nonprofit organization is great. But here’s an even better alternative for high-impact companies with a social mandate: opening their doors so at-risk youth can see success up close, in real time. To learn what it takes to find a good job or start a thriving business. To discover where their skillset will be best used and most appreciated. To understand why they don’t have any time to waste in a highly competitive (and AI job-shrinking) labor market. You see, a lack of vision is arguably the biggest reason why young people from disadvantaged backgrounds check out. At school. On cue. In life. They often have nothing to look forward to regarding favorable outcomes in the future, which is why their interest capital is usually spent on what makes them feel good at the present moment. Here, their mood drives their mode. In other words, feelings (and not values) serve as their de facto guide. That’s a bad place for anyone to be, let alone a young person with a malfunctioning internal navigation system.

Solving problems. Following instructions. Producing results. Assessing (and taking calculated) risks. Maximizing opportunities. Controlling emotions. Handling pressure. Completing projects — on time and within budget. Working efficiently. Collaborating effectively. Communicating clearly. Embracing change. Inspiring others. Recognizing (and preventing) mistakes. Developing talents. Giving back. Dreaming big. These are the “soft” and “hard” skills employers expect, among others, from today’s multifaceted employees. And targeted brain development in these skill-building areas — inside and outside of traditional schooling — is critical to helping disadvantaged youth get up to speed in a dynamic and ever-changing employment landscape. Check this out. A shortchanged child needs a shortcut-providing mentor, or life-changing experience, to make up for lost ground. Vulnerable students, in the majority of cases, are way behind academically and inspirationally. Multiyear academic deficiencies and multigenerational systemic inequities are hard, if not impossible, to close without a bridge-building catalyst in place. Enter unforgettable field trips to area businesses to help connect the relevancy dots. Let me explain.

Although a lot of work for LFYO and our business partners, it is well worth the effort. On our end, we must align in-class activities with real-world applications before going on field trips. Without context, inner-city kids are totally lost in translation. No frame of reference, no short- or long-term buy-in. The result? Opportunity wasted, and worse, the learning experience will likely be immediately stored under the “pain avoidance” category in their amygdala, also known as the emotional memory center. That’s why we use sensory-based learning modalities (in the form of customized PDF games on iPads) to draw youth in. Overlay the fun, underlay the fundamentals — as in lessons learned, knowledge gained, and dream(er/ing) restored. For disadvantaged students, the field trips should be an engaging, exciting, and empowering experience.

With engagement, make them feel welcome the moment they enter the building. In fact, meet them outside just as they’re approaching the front door. Throw on a radiant smile. Offer a handshake (or dap if you’re a germaphobe like me), followed by an upbeat introduction. Remember: It’s your responsibility to establish the oxytocin bond right from the onset, not theirs. For some businesses, excitement is the hardest thing to pull off. Sorry traditional banks, engineering firms, and manufacturing companies, to name a few — I’m just saying. Don’t fret; be creative. Limit the lectures (that will lead them to boredom) … pass around the fixtures (that they can hold as future product designers) … highlight the features (that they’ll one day have access to as investors or homeowners) … allow the gestures (that they can freely express without being judged). Engagement is good, excitement is better, but empowerment is best. Empowerment is the litmus test for every field trip experience, which may take days, weeks, months, years, or decades to pay off. When it happens, attitudes improve, perspectives shift, and behaviors change. Yes, this is easier said than done. Again, it’s a lot of work, but there is a workable solution to closing the opportunity divide in America. One-third is on their frontline support system (caregivers, family members, and educators), one-third is on us (nonprofit organizations, social service agencies, and community-minded investors), and one-third is on them (at-risk youth).

Want to see our students in action? Hit the play button to watch a short recap video of our recent field trips to area businesses!

With limited space, I can’t highlight every one of our 40 business partners (and we need more!), but here are a few of them. First up is AutoTool Inc., an equipment and automation manufacturer. I’ve known Jason Moore, the CEO, for over forty years. He was one of the first white suburban kids here in Central Ohio to hoop, and hold his own, on an AAU team with black inner-city players. Well-spoken, well-dressed, and well-liked, he greets every teen by name at the front door. Jason provides a delicious lunch for the group, gives them a tour of the facility, and allows participants to ask lots of thought-provoking questions. Kim Bodrick is a client-experience manager at Continental Office, which offers full-service solutions for commercial interiors. Kim’s lively personality and friendly demeanor eases participants’ fears, who initially, aren’t quite sure what the experience will entail. After a brief tour of office space layouts to gain inspiration, the youth are placed in their respective teams. While competing in Kim’s Designer Challenge Game, disinterest vanishes and creativity picks up as the vulnerable teens design their office space masterpieces. Each team presents their finished project to the entire group, with bragging rights and prizes up for grabs. This two-hour field trip goes by so fast!

One of our newest partners is ArtNewCo., a whimsical vintage art boutique owned by entrepreneur and art lover Hannah Gleason. With over 800 pieces of rare vintage art and jewelry, ArtNewCo. offers a range of affordable price-points for even the most cost-conscious customers. Hannah invited our group into her studio this summer for a painting activity It was a life-changing experience for many of our teens, in some cases, doubling as a therapy session to move beyond their pain. For that 75-minute window, they didn’t have a care in the world. Musicians were also brought in, a keyboardist and violinist, for biochemical-boosting and circadian-rhythm purposes. Last but certainly not least is The Columbus Foundation, one of the top 10 community foundations in the United States, serving thousands of individuals, families, and businesses with their unique funds and planned giving efforts. Hosted by Steve Moore, Chief of Staff at The Columbus Foundation, he shares with our teens what philanthropy is, why it’s important, and how they can even become philanthropists right now using their time (as community volunteers) and talents (as peer-to-peer mentors). Of course, receivers should at some point transition to givers; the countdown is on. Click the link below to view a comprehensive list with background information on LFYO’s 40 Business Partners:

2025

LFYO Community Partners

Click the link below to view the full list of our community partners.

In closing, here’s how you help under-resourced youth dream big in spite of their current challenges or past failures. First, take the time to understand the roots and offshoots of generational poverty from an empathy-assimilation point of view. Place your physiological self in their physical shoes. The complexities of economic distress are multifaceted and cannot be reduced to a simple explanation. Its branches extend far and wide, including but not limited to structural barriers, psychological disorders, physical disabilities, societal biases, nutritional deficiencies, relational hardships, educational setbacks, and spiritual hangups. Second, assist high-need students in compiling an ownership checklist of synonyms and catchphrases that clarify and crystallize what it means to dream big. Among others, they include “thinking outside the box,” “challenging the status quo,” “defying the odds,” “chasing limitless possibilities,” “reaching for the stars,” “aiming high,” “setting bodacious goals,” “having a driving ambition,” “thinking big and bold,” “aspiring for great things,” and my favorite, “never settling for less” when more is available. More progress. More success. More happiness. What is an ownership checklist? This to-do list or schedule of activities can place students in the driver’s seat, where they’re in control of their respective dream — as they imagine it. In effect, this list holds students accountable for their growth gains in thought, word, and deed. Third, provide vulnerable youth with unforgettable field trips and life-changing experiences that can enlarge their possibility filter. In this article, I’ve shared a working template that you can follow or modify to your satisfaction. Let’s move out so they can move up!

Letters from LFYO Business Partners

Ascend Advisory Group

Tony Reilly

CEO

Hamilton Parker

Laura Wagner

Director of Human Resources

Schottenstein Real Estate Group

Kerri Ward

Director of Corporate Marketing & Communications

This is a very long headline to turn your visitors into users

Change the color to match your brand or vision, add your logo, choose the perfect layout, modify menu settings and more.

Medium length display headline

Change the color to match your brand or vision, add your logo, choose the perfect layout, modify menu settings, add animations, add shape dividers, increase engagement with call to action and more.

Short headline

Change the color to match your brand or vision, add your logo, choose the perfect layout, modify menu settings and more.

LFYO 2025 Summer Programs

LFYO has teamed up with the GoodLife Foundation and Gladden Community House to present seven weeks of summer programming for area youth. For vulnerable populations, it’s critical to offer positive outlets to combat their often negative outlooks. One thing is certain: We must keep our kids safe and out of harm’s way, just as warmer days tend to lead to more community violence. Financial life skills not only improve favorable outcomes for at-risk youth, but they also serve as violence prevention measures. You see, the biggest difference between disadvantaged teens and their well-to-do peers comes down to opportunity. Highly successful careers are par for the course in affluent (and even upper middle class) communities. And this is why their children have a distinct advantage. That’s why LFYO serves as a bridge-building specialist to help level the playing field without settling a score. By leveraging the three E’s of success, this can help close the opportunity gap. Exposure. Experience. Expectation. Expose underserved youth to what can be, provide the life-transforming experience to achieve it, and watch what happens. The expectation to do better feeds itself when they’re fed a smorgasbord of real-world opportunities (which is a beautiful thing to behold when at-risk youth who once felt disempowered now value empowerment). This is how we change lives and transform legacies, one broken spirit and battered soul at a time.

Destiny is something you can’t run from or bump into by accident. Either you’ll fulfill it or let it waste away.

Over the past four weeks, we’ve taught underserved youth how to create (and protect) their personal brand, identify their unique wiring fit, and gain much-needed financial life skills. Heavy concepts indeed for teens and tweens to grasp. But young people can learn anything if it’s memorable, manageable, and marketable to their way of thinking. What’s memorable draws upon hope. What’s manageable provides the help. And what’s marketable fuels the hype, or what it takes to get them fired up about their promising future. Chris Scott, general manager at Toy Barn Cars, commented, “The group of kids you brought in for a tour last month were very impressive. They asked great questions, which is a sign that they’re serious about their future!” Jennifer Griffith, market president of First Merchants Bank, shared, “Your kids came up with some really clever ideas in the Shark Tank simulation game during their visit to the bank.” She added, “And many of them seemed to overcome their fears of public speaking, which is tough for adults let alone children to do.” It’s not a capability issue with our most vulnerable youth; it’s an accessibility problem. When they’re armed with an upgraded vision and a rock-solid value proposition, their upside is limitless. Take a look at the pictures, videos, and lineup of LFYO’s summer activities thus far …

Hope

The measures employed by LFYO to assist at-risk youth in fine-tuning their faith lens while in pursuit of a promising future.

Help

The means offered by LFYO to empower vulnerable populations through life-changing experiences and cutting-edge programs.

Hype

The methods used by LFYO to get inner-city youth fired up about their future opportunities as well as the work involved.

Video Highlights

Please take a moment to view a brief video highlighting some of the key moments from our initial meetings with the participants.

2025 Fundraising Luncheon

The 2025 LFYO Fundraising Luncheon is just around the corner. It will be held once again at Hyde Park Prime Steakhouse (Downtown). The date? September 12th. The time? 11:30 AM to 1:30 PM. The cause? To raise investment support for LFYO programs. The offering? A first-class experience at a five-star dining establishment while mixing and mingling with some of Central Ohio’s most prominent and influential people. The crowd? Business leaders, former Ohio State coaching legend Jim Tressel and other Buckeye greats as well as philanthropic-minded individuals (like yourself) will be in attendance. To date, we have almost 30 committed sponsors — a record. If you or your organization is interested in sponsoring or attending the event, please email me at info@MrFundy.com. Couples and individuals with an interest in attending the 2025 LFYO Fundraising Luncheon will be placed on a waiting list due to limited seating of 140 attendees. First preference is given to sponsors and their guests. For more details on the event, please click the button below.

The Location

Hyde Park Prime Steakhouse (Downtown)

The Time

11:30 AM to 1:30 PM

The Offering

A first-class experience at a five-star dining establishment while mixing and mingling with some of Central Ohio’s most prominent and influential people.

The Date

September 12, 2025

The Cause

To raise investment support for LFYO programs.

The Crowd

Business leaders, former Ohio State and ex-professional athletes, and philanthropic-minded individuals (like yourself) will be in attendance.

In closing, we want to once again acknowledge our 2024 and 2025 Legacy Sponsor, Maggie and Tom Fleming. Their generous contributions have allowed LFYO to purchase more than 30 iPads with bluetooth keyboards and protective cases as well as offer programs free of charge to hundreds of inner-city youth. To the Flemings — and every LFYO investment supporter! — thank you for helping us carve out our unique niche in changing lives and transforming legacies here in Central Ohio and beyond.

Upstream Problem, Downstream Playbook (Part Four)

Hype fizzles and hope fades without the help. To whom much is given, much more is required. And when you see a need and don’t fulfill it — ardent capitalists, I’m speaking to you! — a lot of innocent people get hurt (and left behind) in the process. Now, capitalism gets a bad rap when certain segments of society who have less begrudge, and sometimes berate, those who have a whole lot more. Obviously, it’s nearly impossible to move up the socioeconomic ladder when you have tremendous disdain or utter contempt for those who’ve legitimately climbed to the top of it. These ladder climbers have worked hard, played by the rules, and taken the necessary risks to generate wealth. No harm, but why are they being called for a foul? Without question, capitalism has its fair share of embedded flaws, and they’re too numerous to cover in this article. But this flawed system is still the best option we have among competing alternatives, notably socialism, collectivism, marxism, egalitarianism, and transhumanism. Without access to capital, it’s easy, really quite natural, to take issue with the excesses of capitalism.

I get it. Equal opportunities do not always translate into equitable outcomes. This is where the haters of capitalism miss the mark, demanding that the government step in and legislate social outcomes based solely from the lens of economic justice. Serving as the de facto referee to mitigate wealth inequalities is a slippery slope for any governmental agency to oversee. In sports, the best referees are those who aren’t noticed, no matter where the game is being played — at home or on the road. They intervene only when the “right call” requires it, independent of the background noise. As a compassionate capitalist myself, we’re free to earn a great living individually or entrepreneurially, so long as we’re good stewards of the planet while empowering the least among us in lockstep with our money-making endeavors. Arms-length donors are good, where high net worth individuals and families write sizable checks to charitable organizations. However, in-person philanthropists are best. They’re not afraid to fund worthwhile causes and embrace sociophilanthropy, where mega-affluent Americans reach and teach the less fortunate, on their court, how to build legacy wealth. One income stream or investment asset at a time.

An Opportunity (and Free Meal!) Too Good to Pass Up